Initiative Q - Money from nowhere?

-

@groaner said in Money from nowhere?:

I yearn for the day when PR people can insult back when they have the moral high ground, but I don't think that's going to happen in our lifetimes.

I don't think the bolded part is going to happen.

-

@dcon last time I used one (in an apartment facility), they had cards that you could load with money. Except the setup was asinine:

- get card.

- register on website

- use card to add money, receive alphanumeric code

- go to laundry facility, stick card in special box on wall. punch in code to actually load the card.

- use the card.

IIRC, it had a limit like $20, so about a month's worth of laundry (two loads a week, 3 bucks a load).

It was obnoxious--almost as bad as having to get quarters.

Edit: that was about 4 years ago.

-

@chaostheeternal said in Money from nowhere?:

And here's my link: https://initiativeq.com/invite/SxvqfiUW7

I'm signed up using your link, because I, too, am somewhere between gullible and optimistic.

-

@cursorkeys said in Money from nowhere?:

@blakeyrat said in Money from nowhere?:

- Get a critical mass of users, who join only for the free Qs

- ???

- Profit!

I'm guessing step two is 'show outside investors a large number of 'live' users to secure investment and pay salaries'.

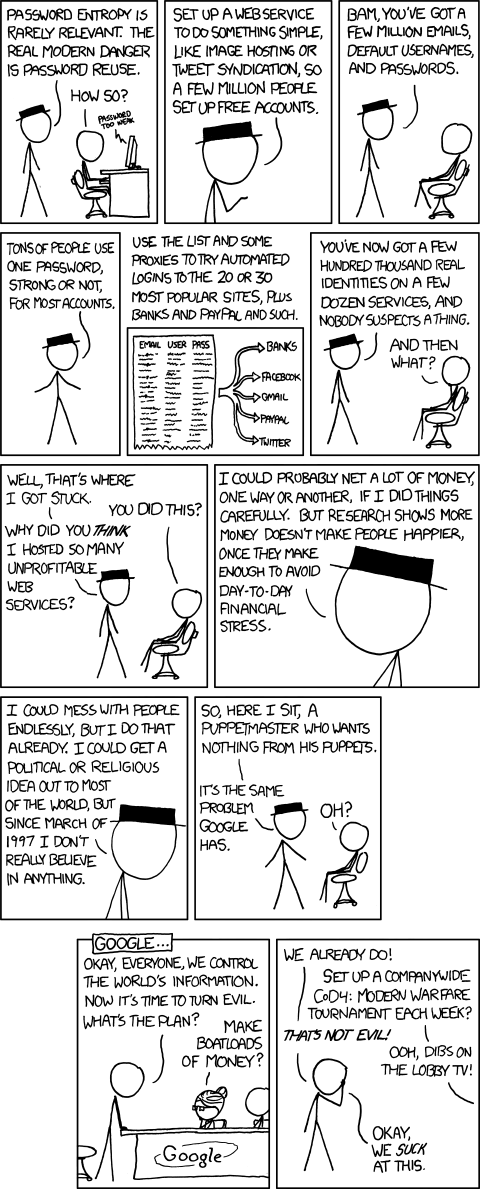

I'm guessing step 2 is "Exploiting password reuse."

Because XKCD never gets old, right?

-

@potatoengineer No email notification that you signed up on my link, I'm guessing they expect it to be the "hey I give you this link and you sign up immediately" kind of inviting instead of what we're doing. Glad you said something in topic or I probably wouldn't have noticed until tomorrow.

Only 4 more to go... to hit the second set of "invite

suckersyour friends and other interested parties"... which I'm sure I wouldn't be able to finish, even if they gave me 72 days.

-

@chaostheeternal said in Money from nowhere?:

Glad you said something in topic or I probably wouldn't have noticed until tomorrow.

They do dispatch an email eventually, like, after an hour or so.

-

@chaostheeternal said in Money from nowhere?:

@potatoengineer No email notification that you signed up on my link, I'm guessing they expect it to be the "hey I give you this link and you sign up immediately" kind of inviting instead of what we're doing. Glad you said something in topic or I probably wouldn't have noticed until tomorrow.

Only 4 more to go... to hit the second set of "invite

suckersyour friends and other interested parties"... which I'm sure I wouldn't be able to finish, even if they gave me 72 days.ding! ding!

-

@groaner said in Money from nowhere?:

Yes, because there are these things called laundromats, parking meters, vending machines, and arcade machines (to name a few) which still haven't migrated to more modern payment options and probably won't for some time yet.

Some of them have converted. There are laundromats that use smart cards; I have two of them that are no longer useful to me because I have moved out of the area of the laundromats that issued them. There are vending machines that take credit cards and parking meters that one pays by phone.

Not all of them, though. I still go through a roll of quarters every time I do laundry.

-

@groaner said in Money from nowhere?:

I've seen them as well. Problem is, what about all the meters in Backwaterstan?

We have it for parking meters on shitholistan. I guess it can easily happen in backwaterstan too. It's not rocket surgery.

-

Doesn't look like a scam despite walking and quaking like one, since they don't actually ask for money or anything other than "participation". So let's see.

@initiativeq said in Money from nowhere?:The problem is not competition, but how silly it is that we identify our accounts with a large piece of plastic

What exactly is silly about credit cards being made of plastic? Have you actually considered all the benefits they afford, or do you simply think that anything old must be silly? Consider, just for starters, that credit cards don't require that you have a smartphone with a data plan. When one of the hurdles you're trying to overcome is "barriers to entry", it's hard to beat a piece of plastic.

Credit cards are suboptimal, causing sellers to resort to technology that is thousands of years old (cash).

Again, old doesn't automatically mean bad. It may be inconvenient, but the older thing works as a fallback for the newer thing, for when even the shop's connection drops, for example. How does Q solve the problem of a shopper's data cap running out, or the shop's internet connection being bad? Cash provides a physical token that the shopper and seller can hold on to until they deposit it in the bank. Until we reach the situation where the whole world is blanketed by cheap, reliable, wireless internet, you're going to need cash sometimes.

Just an example. The point is that if you were free to design a payment system from scratch, without worrying about critical mass, you would come up with much smaller and more secure ways to identify an account.

Credit cards aren't that size because they NEED to be that size. They could be much smaller. They're that size because it's a size that is easy to handle. Technologically, they could be a couple cm^2 and the chips and NFC tags would still work. Make them considerably smaller however, and you can easily misplace them or waste time trying to sort them out. It's not a coincidence that they're about the size of a business card.

As for security, chip cards at least are about as secure as a phone can reasonably be (need to know a pin to unlock), and more importantly, don't run out of batteries.

True for some, but not for all. Do you really think that if we were free to reinvent payments, people will be walking around with round pieces of metal in their pockets?

Again, it's a matter of reliability. For example, a CD can theoretically hold on to information for about a decade if I recall correctly. In practice, they're already obsolete. Paper can hold on to information for thousands of years, and won't become obsolete until people stop having eyes. If there's a global catastrophe that knocks down the energy infrastructure, all the information in all our servers will be inaccessible, while all the information in outdated libraries will be perfectly available. Coins have the benefit of being pretty sturdy. A coin will go through the washer in your pocket and be just fine afterwards. Most currencies won't (Canadians I think have some kind of plastic money that can be washed). More importantly, they don't need to be replaced so often, so they have a low maintenance cost compared to paper bills, and they serve as a backup for when the fancy tech fails.

- Then you can build a superior payment network without worrying about adoption.

This is I think where you lose me. It's ok to have a lot of people with Qs, eager to use them. But who is going to accept them? At what exchange rate? Government currencies have the advantage that you have to pay your taxes in them, so everyone needs the currency of their country no matter how crap it is, because if you don't pay taxes you eventually (if you are poor anyway) go to jail. Also, governments enforce that their currency is a valid means of exchange, and kind of force shops to accept it. The other alternative is if you live in a closed community where people ONLY have access to a certain currency, so sellers have to accept it because they can't do business otherwise. See cigarettes in prison, for example.

So what's moving first sellers, who by virtue of being the first have no one to unload them onto for the goods and services they require, to accept Qs?

- When you design a payment system correctly, you can reduce transaction costs to a fraction of what they are today.

What do you think the actual transactions costs for VISA and Mastercard are? And I don't mean what they charge, they charge what they can get away with. I mean their actual costs for having their servers running fraud analysis, routing to banks, and approving or rejecting transactions. Do you have a figure?

-

Ultimately, I don't know if anyone has said this before yet, but if you have an idea for such an amazing payment system, why bother with the new currency at all? VISA and Mastercard handle all kinds of currencies, and you can largely use one credit card with one currency in any place, with the card and banks dealing with the conversions for you. The rates aren't always great, but they're not awful either.

These are two completely separate issues. You don't need a new currency to make a payment system. A good payment system would work with any currencies transparently.

-

@kian You don't want yourself some Q's ?

-

-

@initiativeq said in Money from nowhere?:

Why carry anything other than my smartphone?

Fuck you, give me money

Fuck you, give me money

Okay, um--- umm..

umm..

Time to break some kneecaps

-

@twelvebaud said in Money from nowhere?:

- one global currency to eliminate currency exchange fees - Is this an actual problem?

Have you never bought anything from overseas?

@pjh said in Money from nowhere?:

I just found it amusing that the newbie who hasn't lurked enough to get the meme Blakey was alluding to, was accusing Blakey of

I read it as admitting to their own

, not accusing Blakey of it.@e4tmyl33t said in Money from nowhere?:

Being less facetious here, but that's actually something I see in all the cyberpunk stuff I read/watch/whatnot that I think SHOULD happen. Not an app, necessarily, but having a single digital ID device that things like licenses, accounts, and everything get linked to so the only thing you need to have is the ID device.

Ah, like the Identi-Eze from HHGTTG? So that anyone who can get hold of it can instantly steal your identity (as Ford does in the novel)?

-

@weng said in Money from nowhere?:

My wallet contains 6 payment cards.

It also contains 2 forms of government ID (the one that lets me drive and the one that lets me use land borders), a corporate ID, 3 different membership cards for getting healthcare, a payment card for healthcare, a membership card for a gymimma stop you there.

All those neat pieces of ID that effectively lead to some very personal information about you?

Yeah-- I don't want that information anywhere near a corporate entity, let alone a gym.

A single ID means giving everyone all your infos on everything. And if you think "a good ACL / permission system will keep information segregated", I'll remind you which site you're posting that response on.

-

@boomzilla said in Money from nowhere?:

Why use my smartphone to buy stuff in the first place?

How do you buy your first smartphone?

-

@boomzilla said in Money from nowhere?:

Your "verification" stuff is just that people are...people.

yo, I got a whole collection of "verified" IDs here. I just need to dig them out of the mound in the backyard and make sure I didn't get fingerprints on them.

-

@lorne-kates said in Money from nowhere?:

@boomzilla said in Money from nowhere?:

Why use my smartphone to buy stuff in the first place?

How do you buy your first smartphone?

Everyone is issued with a basic iPhone at birth

-

@lorne-kates said in Money from nowhere?:

How do you buy your first smartphone?

Speaking for my kids: your parents buy it for you when you graduate from primary school.

It's worth noting that those of us without drivers' licences face similar difficulties in buying stuff (and certain other activities) from time to time. Which is why the phone account, utilities, etc. are all in my wife's name (well, she also had more free time than I did to set things up when we moved last).

Granted, there are ways to get around that with alternative forms of ID; but this is, from what I've read, not completely effective, as sometimes people who are not used to the alternatives refuse to accept them.

-

@masonwheeler said in Money from nowhere?:

ve seen parking meters that accept cards. They're not common yet,

Uh? Parking meters that only except coins seem to be going extinct fast on this side of the pond.

Most even use SMS or a parking app for payment.

-

@hardwaregeek said in Money from nowhere?:

parking meters that one pays by phone

I haven't seen one that doesn't have this for years over here. There might be some still, but I don't know of them. Parking garages also take credit cards AFAIK.

The only place I know of where you still need cash without an extra piece of hardware are toll booths on highways (makes sense they want to make it fast so they don't have to hand you over a keyboard to put a PIN in, though with contactless cards this might've changed, I haven't asked). The alternative for those, however, exists. You can get a device to put in your car and it will communicate with the toll booth and open the ramp for you automatically as long as you have credit remaining. You technically don't even need to stop with those (which is why they didn't go for cards I guess, it speeds stuff up).

-

@onyx said in Money from nowhere?:

toll booths on highways

have cards around these parts (Netherlands, Belgium & France)

-

@initiativeq said in Money from nowhere?:

Again, the technologies are well known. It's getting people to adopt them that is hard.

Not very i mpressive sidestepping of the question: How are you going to get people to adopt it?

VISA has the leverage of an already existing base of buyers, sellers and creditors they can push into a new network by a host of well known methods they've used before to push new features.

You don't even have an idea of how to build your system as per your own answers in this very thread, so you have less than fuck all to work with to get a new network going.

-

@luhmann we have these:

They call them ENC, or, when translated from Moonlandian, "Electronic Toll Payment". I'm buttuming they went with that over cards because we do have some chokepoints here, especially during summer when tourists rush in, so even the small amount of time saved by not having to stop, roll down the window and scan the card (both when entering and leaving the toll road) adds up to a decent amount of time when it's plenty of people going through. Because this isn't uncommon in the summer:

Cash is still an option if you don't want to mess with the device, of course. Also,

I think this is an old photo(yeah, it says 2003 on it, I'm just blind) before they added the lanes for the electronic thing, if I could find a newer image you'd see 2 or 3 lanes pretty much empty in comparison.

-

@hardwaregeek said in Money from nowhere?:

@initiativeq said in Money from nowhere?:

VISA don't need us to tell them about it. They already know how to do it, but they can't, because it requires building a new network from scratch, and they don't know how to get everyone to move to the new payment network.

That seems improbable. ISTM that if a payment processor with the reputation and clout of VISA told their merchants, "We're setting up a new network that's more secure and with lower fees," there would be a stampede to the new network. Customers would be forced to move, because eventually the old one would stop working.

Why would there be a stampede? What's the rush? Every seller will wait to see that others are moving, before making the investment.

-

@onyx

France has a similar system. Netherlands & Belgium have very few toll roads, both only on 1 tunnel that I am aware off. So here it is more limited.

Thinking of it both tunnels only make a profit because they allow you to circumvent the mess that is called 'Antwerp'

-

@luhmann said in Money from nowhere?:

tunnels only make a profit because they allow you to circumvent the mess that is called 'Antwerp'

Yeah, we kinda need them here for the purposes of circumventing the mess that is called "fucking huge mountain, where the fuck is the top already?"

-

@groaner said in Money from nowhere?:

@initiativeq said in Money from nowhere?:

The problem is not competition, but how silly it is that we identify our accounts with a large piece of plastic.

That seems like mostly a philosophical objection. I think it's silly that men put on helmets and spandex and give each other brain injuries while moving a pointed, egg-shaped piece of leather down a grassy stretch of land, and that members of the public express extreme anguish over any injuries said men in helmets and spandex might suffer. But as much as it's irrational to me, it exists.

Well, sports is different. It's entertainment. Here we are talking about business. You're trying to be as efficient as possible.

Just an example. The point is that if you were free to design a payment system from scratch, without worrying about critical mass, you would come up with much smaller and more secure ways to identify an account.

But as a developer, I'm intimately interested in the critical mass situation, especially if it's my job to deliver a functional system. Handwaving does not produce stable, high-availability, secure systems that can handle the kind of traffic you guys are aiming to attract.

The idea is to bring the best minds in the payment industry to work in an environment where they aren't burdened by critical mass limitations. So first we need to create that environment.

I have also seen many young developers (and been one myself) who were too keen to throw away something old and covered in warts, replacing something functional with something that has a ton of bugs (as all new software does), and then made many of the same mistakes their predecessors made (and then fixed) in that old, ugly code.

We're definitely not dismissing everything just because it's old. If you read through our papers, you can see that in many cases we are choosing to copy concepts from credit card networks and government currencies.

Actually, there is very little use of advanced fraud prevention algorithms in today's payment networks. Interestingly, many of the innovations in the field were made by Initiative Q's founder, Saar Wilf (founded Fraud Sciences, acquired by PayPal).

How do you know this? Have you examined the algorithms in use by many of the big players today? Would they so readily share their secret sauce with you?

There is constant movement of talent between the leading players in the field, so everyone knows what the others are using. Of course, the specific models and code are secret, but the approach and technologies are well known.

True for some, but not for all. Do you really think that if we were free to reinvent payments, people will be walking around with round pieces of metal in their pockets?

Yes, because there are these things called laundromats, parking meters, vending machines, and arcade machines (to name a few) which still haven't migrated to more modern payment options and probably won't for some time yet.

They would upgrade quickly if all consumers had an alternative they preferred.

One of my hobbies is 1/4 mile drag racing. It's rare you will even find a functional ATM at a dragstrip. They are effectively all cash for admissions and concessions. What's your answer to that?

Not familiar with this exact scenario, but I assume a smartphone-to-POS, or smartphone-to-smartphone transaction would work.

Don't follow your point. Do you disagree that a hypothetical superior network with wide adoption would process trillions of dollars a year?

We can debate that when such a network exists.

How do we get there?

- Get a critical mass of users, who join only for the free Qs.

- Then you can build a superior payment network without worrying about adoption.

- Everyone prefer to use it because it's cheaper, faster, safer.

- Qs have value ("the equation of exchange")

I think steps 2 and 3 are going to be much harder to implement than you think, and it concerns me that you're handwaving away the details. Now, if you guys do have a detailed plan for that and don't want to disclose it for obvious reasons, that's great. More power to you. But I would think if you had solved the hard problems already, you'd be taking a different approach than hypotheticals.

We actually think steps 2 and 3 are very difficult. But step 1 is what makes them maybe possible. If there was certainty they would succeed a Q would be worth close to $1 today...

There are of course many plans we didn't yet publish, but to be modest - most of the innovation will come in the future from bringing the best talent in the industry. And for that, we need to achieve step 1.Note that all users in Initiative Q must be invited and verified by an existing user. In the future, all users will undergo additional verification, and people who approved fake users will lose their rewards. This reduces the ability to claim multiple incentives - not to zero, but close to it.

I have a feeling that most of the regulars on this forum could easily defeat whatever countermeasures are in place. VPNs are a thing. Email addresses are easy to get. Throwaway SMS numbers are easy to get. The good news is that if you manage to pull it off, Google and Facebook would probably be banging down your door for your technology as even they can't prevent fake accounts.

Not claiming to prevent fake accounts. Just to dramatically reduce them to a manageable level.

- When you design a payment system correctly, you can reduce transaction costs to a fraction of what they are today.

- Definitely possible that we will have competitors. We'll just have to try to be the best.

Well, you've got your work cut out for you. Failing that, you'll still have a nice database from which you could sell user analytics.

That is definitely not the intention, and against our privacy policy.

-

@onyx

:mountain_envy: I have to drive > 1h to go to somewhere with gentle hills

-

@jaloopa said in Money from nowhere?:

@initiativeq once you have your millions of people signed up, how are you planning on getting them to spend their Qs? Say I'm an early adopter convinced this currency is eventually going to be worth a similar amount to US dollars, why would I spend it when it's worth a fraction of that? If it's all about velocity of money you need people to want to get rid of it rather than hoarding or speculating

This is explained in "Economic Model". Your Qs will not be available for use at once, they are released gradually, maintaining a value of around $1.

-

@jbert said in Money from nowhere?:

@tsaukpaetra said in Money from nowhere?:

@mott555 said in Money from nowhere?:

So in this thread everyone accuses Q of being a scam, but joins in just in case it isn't? Do I have that right?

It's free, why not?

"If the product is free you are not the customer, you are the product"

Usually true, but not in this case. Here the value comes from creating trust in a new currency, not from monetizing the user base.

-

@initiativeq Ben, How do you have time to be on a forum like this when you're trying to get a product off the ground. If anything, Mad respect for time management skills.

-

@stillwater

I guess you have a lot of time on your hands when you have no product to work on. Working on anything will come later, on step X, when we have trust of millions.

-

@kian said in Money from nowhere?:

Doesn't look like a scam despite walking and quaking like one, since they don't actually ask for money or anything other than "participation". So let's see.

@initiativeq said in Money from nowhere?:The problem is not competition, but how silly it is that we identify our accounts with a large piece of plastic

What exactly is silly about credit cards being made of plastic? Have you actually considered all the benefits they afford, or do you simply think that anything old must be silly? Consider, just for starters, that credit cards don't require that you have a smartphone with a data plan. When one of the hurdles you're trying to overcome is "barriers to entry", it's hard to beat a piece of plastic.

Exactly - Initiative Q is about building a payment system that isn't concerned with barriers to entry.

Credit cards are suboptimal, causing sellers to resort to technology that is thousands of years old (cash).

Again, old doesn't automatically mean bad. It may be inconvenient, but the older thing works as a fallback for the newer thing, for when even the shop's connection drops, for example. How does Q solve the problem of a shopper's data cap running out, or the shop's internet connection being bad? Cash provides a physical token that the shopper and seller can hold on to until they deposit it in the bank. Until we reach the situation where the whole world is blanketed by cheap, reliable, wireless internet, you're going to need cash sometimes.

Even if Initiative Q is wildly successful, it would be more than 10 years until it is used everywhere. Wireless internet should be ubiquitous by then.

Additionally, in small amounts you could allow transactions when internet is down.Just an example. The point is that if you were free to design a payment system from scratch, without worrying about critical mass, you would come up with much smaller and more secure ways to identify an account.

Credit cards aren't that size because they NEED to be that size. They could be much smaller. They're that size because it's a size that is easy to handle. Technologically, they could be a couple cm^2 and the chips and NFC tags would still work. Make them considerably smaller however, and you can easily misplace them or waste time trying to sort them out. It's not a coincidence that they're about the size of a business card.

I think most people would prefer to get rid of their wallet and replace it with a single RFID tag on their keychain, or merge into their smartphone.

As for security, chip cards at least are about as secure as a phone can reasonably be (need to know a pin to unlock), and more importantly, don't run out of batteries.

True for some, but not for all. Do you really think that if we were free to reinvent payments, people will be walking around with round pieces of metal in their pockets?

Again, it's a matter of reliability. For example, a CD can theoretically hold on to information for about a decade if I recall correctly. In practice, they're already obsolete. Paper can hold on to information for thousands of years, and won't become obsolete until people stop having eyes. If there's a global catastrophe that knocks down the energy infrastructure, all the information in all our servers will be inaccessible, while all the information in outdated libraries will be perfectly available. Coins have the benefit of being pretty sturdy. A coin will go through the washer in your pocket and be just fine afterwards. Most currencies won't (Canadians I think have some kind of plastic money that can be washed). More importantly, they don't need to be replaced so often, so they have a low maintenance cost compared to paper bills, and they serve as a backup for when the fancy tech fails.

I guess you're right in these extreme cases, but we can do better for the other 99.9%

- Then you can build a superior payment network without worrying about adoption.

This is I think where you lose me. It's ok to have a lot of people with Qs, eager to use them. But who is going to accept them? At what exchange rate? Government currencies have the advantage that you have to pay your taxes in them, so everyone needs the currency of their country no matter how crap it is, because if you don't pay taxes you eventually (if you are poor anyway) go to jail. Also, governments enforce that their currency is a valid means of exchange, and kind of force shops to accept it. The other alternative is if you live in a closed community where people ONLY have access to a certain currency, so sellers have to accept it because they can't do business otherwise. See cigarettes in prison, for example.

So what's moving first sellers, who by virtue of being the first have no one to unload them onto for the goods and services they require, to accept Qs?

Excellent questions, that are discussed in detail in the Economic Model page. One important point is that Qs are released gradually to match economic activity, and can be sold to Q's monetary committee for ~$1.

- When you design a payment system correctly, you can reduce transaction costs to a fraction of what they are today.

What do you think the actual transactions costs for VISA and Mastercard are? And I don't mean what they charge, they charge what they can get away with. I mean their actual costs for having their servers running fraud analysis, routing to banks, and approving or rejecting transactions. Do you have a figure?

Yes. Most of the costs are at the banks, not the associations (Visa/MC), and they are not that far from what they charge.

-

@kian said in Money from nowhere?:

Ultimately, I don't know if anyone has said this before yet, but if you have an idea for such an amazing payment system, why bother with the new currency at all? VISA and Mastercard handle all kinds of currencies, and you can largely use one credit card with one currency in any place, with the card and banks dealing with the conversions for you. The rates aren't always great, but they're not awful either.

These are two completely separate issues. You don't need a new currency to make a payment system. A good payment system would work with any currencies transparently.

Of course, but having a payment network with an exclusive currency is what allows us to get wide adoption.

-

@stillwater said in Money from nowhere?:

@initiativeq Ben, How do you have time to be on a forum like this when you're trying to get a product off the ground. If anything, Mad respect for time management skills.

This is the first forum to discuss Q (remember we haven't officially launched yet, just sent the link to a few friends), so it's a great way for us to collect feedback.

-

@initiativeq said in Money from nowhere?:

@stillwater said in Money from nowhere?:

@initiativeq Ben, How do you have time to be on a forum like this when you're trying to get a product off the ground. If anything, Mad respect for time management skills.

This is the first forum to discuss Q (remember we haven't officially launched yet, just sent the link to a few friends), so it's a great way for us to collect feedback.

Oh yes, this forum is great for feedback.

-

@mrl said in Money from nowhere?:

Oh yes, this forum is great for feedback.

It's like being fed to the lions and almost no one comes back?

-

@mrl said in Money from nowhere?:

@initiativeq said in Money from nowhere?:

@stillwater said in Money from nowhere?:

@initiativeq Ben, How do you have time to be on a forum like this when you're trying to get a product off the ground. If anything, Mad respect for time management skills.

This is the first forum to discuss Q (remember we haven't officially launched yet, just sent the link to a few friends), so it's a great way for us to collect feedback.

Oh yes, this forum is great for

feedback

FTFY

-

@onyx said in Money from nowhere?:

@mrl said in Money from nowhere?:

Oh yes, this forum is great for feedback.

It's like being fed to the lions and almost no one comes back?

It's like being carted around a village fair in a cage, where everyone throws rotten food at you.

Or, sometimes something like this

https://www.youtube.com/watch?v=zrzMhU_4m-g

-

@initiativeq said in Money from nowhere?:

What's your idea for a way to "solve" this problem? Do you tattoo it on my arm?

There are dozens of better identification methods you can run on your smartphone.

I kinda like that that there is no malware that runs on my credit card, and when there's malware on the merchant's terminal that skims data, that's mostly (modulo some bureaucracy contesting transactions) the credit card company's problem.

With malware on my phone, it's much more likely to be my problem.Again, you are agreeing with us: Credit cards are suboptimal, causing sellers to resort to technology that is thousands of years old (cash).

Old != bad.

Are you trying to claim moving coins around is the best way to transfer value?

Apart from the fact that he clearly wasn't, I'm going to claim that it's the appropriate way in many situations. There is no one "best way".

Saturday I went to the lake with my son. I gave him a couple of coins to get an ice cream and a coffee at the kiosk; a minute later he came back with a bruised knee and asked me for another € because he ran, fell, and lost one of the coins.

Thank fuck I hadn't given him my smartphone instead.In a pyramid scheme people pay those who brought them in. Initiative Q is free. The value to early users is from the collective trust in Q - no one pays for it.

It's easy to trust if it doesn't have any actual value. That tends to change when you have to connect it to your bank account or whatever other thing you store the result of your working hours in.

We currently have nothing. But companies like Forter and Riskified definitely have technology superior to BofA. We will use them.

No way that's gonna incur any fees.

-

@initiativeq said in Money from nowhere?:

Qs have value ("the equation of exchange")

except for they actually don't

-

-

@initiativeq said in Money from nowhere?:

@stillwater said in Money from nowhere?:

@initiativeq Ben, How do you have time to be on a forum like this when you're trying to get a product off the ground. If anything, Mad respect for time management skills.

This is the first forum to discuss Q (remember we haven't officially launched yet, just sent the link to a few friends), so it's a great way for us to collect feedback.

My feedback is that it's one of the dumbest things I've ever seen. All of the worthlessness of cryptocurrencies, with none of the independence and guarantees.

-

@mrl said in Money from nowhere?:

@initiativeq said in Money from nowhere?:

@stillwater said in Money from nowhere?:

@initiativeq Ben, How do you have time to be on a forum like this when you're trying to get a product off the ground. If anything, Mad respect for time management skills.

This is the first forum to discuss Q (remember we haven't officially launched yet, just sent the link to a few friends), so it's a great way for us to collect feedback.

Oh yes, this forum is great for feedback.

Well, you get pretty candid feedback, and any flaws (real or otherwise) with your ideas pointed out very thoroughly. :D

-

@kian said in Money from nowhere?:

Doesn't look like a scam despite walking and quaking like one, since they don't actually ask for money or anything other than "participation".

You guys are the backup material that lets them scam money off of venture capitalists.

-

@initiativeq said in Money from nowhere?:

Even if Initiative Q is wildly successful, it would be more than 10 years until it is used everywhere. Wireless internet should be ubiquitous by then.

Powered by fusion!

@initiativeq said in Money from nowhere?:

I think most people would prefer to get rid of their wallet and replace it with a single RFID tag on their keychain, or merge into their smartphone.

Suckers.

-

@initiativeq said in Money from nowhere?:

For example, a CD can theoretically hold on to information for about a decade if I recall correctly.

My experience with cheap chinese recordable CDs is that they get bad within the week

-

@initiativeq said in Money from nowhere?:

For example, a CD can theoretically hold on to information for about a decade if I recall correctly.Much longer if it's manufactured correctly.