Almost going full Lorne Kates

-

No, in The Netherlands, for the part above € 57.585 per year, you pay 52%. That's half your income.

-

Because tax is a thing. Almost every good attracts 20% of its sale price as tax direct to the government.

As for 'poor', I don't find that paying 23% of my total salary in taxes/insurance is actually that huge a burden - and it's all taken before the money gets to me, it's not like I have to set aside any to pay taxes at the end of the year, my employer deducts it from my salary as I get paid. And after that, I'm still very comfortable thank you very much. I'm paid market rates for my PHP stuff, I could make a few thousand more working here in Brighton if I wanted to work on WordPress shite every day.

-

Yeah, as you go further east and north, the taxes go up. But at least you don't have to pay for the time you spent waiting 8 hours on a doctor to look at your sinus infection.

Healthcare is something China gets right. I walk in, a nurse says, "symptoms?", I say what it is, I walk out with prescribed medicine. Less than $10, and 1 min later.

All us westerners break socialism.

-

Don't forget, if your doctor prescribes you medicine here, and you're over 18 (and not in full time education) and not pension age, you'll pay for the prescription in England at least and it's something like £7.40 per drug prescribed.

-

my total income tax plus national insurance (healthcare, unemployment etc) comes to about 23% of my total income.

Mines 28% of total and I'm still paying my student loan on top of that.

The student loan is, at least, done in January.

-

I don't have student loans, never did the uni thing. Also, you're earning more than me. But I'm just a lowly PHP programmer

-

Wow....

Half your income....

Protip:Last year I did some maths. I categorized every dollar that passed through my bank account and pay stubs, added up all the money that got sucked out of me on taxes and other government fees (including sales tax, fuel taxes, etc.) plus all the stuff that would be provided for me in a European style socialist economy (healthcare, education, basic retirement). It came out to 53.4% of my gross income.

In America, we just privatize our high taxes.

-

No, in America we're double dipped.

They want to tax us for stuff, then can't half produce the social systems in Europe, and thus we pay twice for the same thing.

The reason I don't want the social systems, is because the American government has failed to adequately produce any of them.

Our new healthcare changes resulted in this change.

Before:

- The rich never had to worry about paying for healthcare.

- The middle class had robust health insurance.

- The poor had little to nothing.

After:

- The rich still do not have to worry about paying for healthcare.

- The middle class gets high deductible insurance, but their jobs soak up a lot of the damage. They pay higher for healthcare than before because the elderly are paying less.

- The poor get super high deductible insurance that pays for nothing until they meet the high deductible they can't meet.

Good job.

You made it worse for everyone, just to do nothing for the poor.

It's no wonder the insurance companies were excited about the new laws.

It meant more premiums and less payouts.

That's after considering their registration website was a joke that failed all the time, and yet they still threatened the people who didn't have insurance when the main reason was that they couldn't get the website to work.

And you want me to trust them with single payer?

-

It's easy to have good ideas.

It's not the ideas I'm worried about.

It's the execution of those ideas.

-

Yeah, but you guys pay like 60% income tax.

Marginal rates, after nill-rate bands

Income tax: (10% special case - few people pay this), 20% (the typical), 40%, 45%

Employee's National insurance (income tax in all but name): 12%, 2%

Employer's National insurance (employee effectively bears this): 13.8%So your typical worker's salary generates (marginal rates of) either 20%+12%+13.8%=45.8% or 40%+2%+13.8%=55.8%.

Then the government does some double and treble dipping with VAT of 20% on most stuff and excise duty (calculated after VAT added, naturally) on stuff like fuel(~60%), nicotine(70-90%) and ethanol (~5%-70%).

-

Before (revised):

- The rich never had to worry about paying for healthcare.

- The middle class had robust health insurance.

- The poor had little to nothing.

- If you had any kind of pre-existing condition, coverage was not available at any price. If by some miracle you did manage to wangle coverage, you were knocked out of the plan at first excuse they could find for rescission.

After (revised):

- The rich still do not have to worry about paying for healthcare.

- The middle class gets high deductible insurance, but their jobs soak up a lot of the damage. They pay higher for healthcare than before because the elderly are paying less.

- The poor get super high deductible insurance that pays for nothing until they meet the high deductible they can't meet. This is an improvement over no coverage.

- Those with preexisting conditions get super high deductible insurance that pays for nothing until they meet the high deductible. This is an improvement over no coverage.

Arguably, it got worse for the middle class, assuming they don't have an employer plan. And, what evidence would anyone give that coverage got worse for the rich? That leaves the poor, and you're asserting that the fact they can only get bad plans, is worse (or at least no better) than having no coverage at all.

That is a desperately weak argument.

-

nicotinetobacco products(70-90%)And thank God for that, since it makes my habit so much less expensive.

-

and you're asserting that the fact they can only get bad plans, is worse (or at least no better) than having no coverage at all.

I'm arguing that the net effect for the middle and poor class is negative.

Look, I know some people give fuck-all about the middle class and want to do everything for the poor class at any expense.

But I'm not one of those people.

I'd rather spend the money on getting the poor out of poverty, then spending the money on making sure they stay there, and giving them token insurance, that in fact does nothing, and marketing it like free healthcare.

So label me an ass.

But doubling and tripling insurance rates for the largest group of insured prior to the change, to pay for "pre-existing conditions" for the poor that they still can't afford anyway, is in no way an improvement in the vast majority of practical real-life situations. It's a token improvement, at best. A cheap smile and a nod and a pat on the back.

Did you know that pre-existing conditions was hardly ever a problem. It sucked when it did happen, but even if you changed jobs and changed carriers, there were already laws in place to protect your coverage.

While many small business owners had to close shop and get a job, because they couldn't afford the increased cost of coverage. No matter what the paper said, the real-life situations played out much differently. No Mr. President, hardly anyone got to keep their insurance.

And the fact that people are satisfied with what's on paper and never bother to look into the net effects, makes me concerned about what the politicians are yelping about now on both sides of the aisle.

-

So your typical worker's salary generates (marginal rates of) either 20%+12%+13.8%=45.8% or 40%+2%+13.8%=55.8%.

It came out to 53.4% of my gross income.

Yep.

and it's all taken before the money gets to me

That's part of the problem.

You never see the money.

And since Common Core means no one can math anymore...

-

In Texas, the current single person deductible went from 6k to 12-13k after the AHA passed for teachers. Teachers that get paid less than other professionals. And not only that, the government covers less of the premium than private businesses.

So, for twice as much premium as they used to pay, they have to pay 1/4th of their salary (on top of the premiums going up 25% on average) before they begin to get benefits. (outside of routine checkup and flu shots and such).

Now tell me, how is that a net improvement, given that we now cover additionally only about half of what we were told were uncovered, and many middle class and business owners chose to pay the fine anyway.

It's solar freaking roadways level of fail. (which of course also got federal grants).

-

Arguably, it got worse for the middle class, assuming they don't have an employer plan.

Have you seen what passes for employer plans these days?

I am MERE DOLLARS away from being better off shopping on the exchange.

-

https://youtu.be/QPKKQnijnsM

Someone ate the middle class, I wonder who..

-

Common Core means no one can math anymore...

...leading to oddities like claims that a person paying less than a quarter of their income in tax is actually paying half their income. It's quite sad, really.

-

...leading to oddities like claims that a person paying less than a quarter of their income in tax is actually paying half their income. It's quite sad, really.

Do you understand the difference between the one value for income tax, and the total taxes levied on a person combined?

In America for a middle class, it's as much as 40% based on where you live. Even though our tax bracket for the middle class for basic income tax is 25%.

However, when you consider county and state taxes, medicare tax, social security tax, utility taxes, sales tax, gas tax, tolls, tariffs, etc. The % is much higher.

This is no different from any other country.

The base income tax is about half the taxes you end up actually taxed.

The joke goes, around May, we say, Now we're earning for ourselves.

-

One mistake it makes, or rather one omission.

They act like it's suddenly gotten worse and compares it to 1970s values. However, before the great depression, it was moving this way. It wasn't the social programs that unraveled wealth inequality, it was the economic collapse.

A slightly different thing happened during our recent recession, where our government bailed out the top richest (that's right, democrats behaving like republicans, imagine that), that the rich class maintained their wealth while the middle and low class lost a great portion of it.

"Working 380x harder"

Well, he just got through saying all these people are investing, and that the lowest % aren't investing at all. This is another flaw in the distribution rhetoric. The assumption that the wealth from the rich comes from their pay. Even if we taxed their pay higher, it wouldn't change all that much. We'd have to implement bracketed capital gains based on income. But what about the person that earns only through capital gains? Those exist. Well, I hit a brick wall. There's literally no fair way to tax these people, other than a wealth tax. And I absolutely disagree with and abhor the concept of a wealth tax. Because it can end up forcing people to liquidate their assets. And if some of that asset is their business, then we're hurting jobs at this point. Wealth taxes are how some countries made the shift into socialism, and nationalized much of their businesses. It is pure robbery.

But why did we start moving this direction?

Well, it was because of industrialization, and the fact that we shifted from primarily business owner class, to a working class. If I own a business, and I want to open a second location, and put in a manager. That manager didn't take the risk of owning a business. And I certainly get no benefit if I pay him half the net. As businesses collect more and more working class under their roofs, and more people shift from business owners to employees, this stilts the pay even more into the reality. I'm not saying that it's fair for the rich to own so much, or even justifying their owning so much. I'm simply saying that the shift from owning your own business to being employed is a major part of the problem.

But if socialism doesn't make it better, and makes it worse, what can we do?

Well, I don't believe that wealth is a fixed object, rather than the liberal mentality. I believe that wealth is created. So, we'd see some benefit to creating more opportunity, and more ownership opportunities, and more investment opportunities. It's obvious that wealth is directly proportionate to investment. Even if that relationship isn't cause-effect related in a direct sense, there's some manner of relationship there.

Secondly, we need to get it out of our heads that one party is working for wealth equality and one party is working against it. It's quite clear that when it comes to wealth equality, both parties have similar results from their behavior regardless of the rhetoric. Liberal social ideas won't work because socialism doesn't create wealth equality.

In real socialist states, everyone is not visible on the charts, like the poorest on these charts, and the government and people related to the government own 99% of the wealth. The chart is stilted even further than our extreme.

"Tax loopholes"

The tax loopholes are the biggest reason that the rich aren't paying their taxes. It's worse than 15%, Google paid less than double digits tax as a corporation to the government.

Unfortunately, rich have mobility, and if you tax them above their willingness to pay, they'll simply move. It's happening in Norway. I don't know about the UK, but it's happening in America for sure. That drives wealth out of the country.

So what do I advocate?

One thing I'd like to look into is finding ways of chopping up businesses in order to create more ownership over employment. It would still be possible to create big things, we'd just have micro levels of business, instead of one incorporate. And of course, each of those levels has to be owned by someone else. If a business gets too large, then it simply can't.

How to accomplish this in reality?

I'm not sure. That's the problem. I know what others are advocating simply doesn't work. It simply masks the rich. High tax countries are an economic timebomb. And they teeter on losing their wealthy entirely.

I just know that if we want to unravel time, then we won't do it by subsidizing employees. We'll do it only through splitting up wealth creation.

-

-

We don't have Common Core.

-

That's a nice soapbox you have there..

Imo "The biggest problem" in both the Eu and us is lobbyism. They bias the politics too far towards big companies.

The scariest example is your prison system. You essentially still have slavery.

I'll somewhat agree with you, but on many points you seem to think it's binary.

There is no problem in taxing capital incomes as regular income, if you don't have any other income.

-

Someone ate the middle class, I wonder who..

Just change your definition of middle class to cover half of your lower class. Thats is how its done here.

-

Imo "The biggest problem" in both the Eu and us is lobbyism. They bias the politics too far towards big companies

I have a fringe theory that it is what makes these places nice.

Look, you have so many big corps lobbying the government, and in average many of their interests match the average citizen.

Here we have a few mafias that rule the entire country undisputed, and they are not worried with the economy, or a functional state.

-

Speaking of climate change arguments, just a reminder that my GoFundMe is still running.

-

Wow....

Half your income....

Their taxes are incremental, like in the US. I don't know what their highest bracket is, but I assume if any portion of your income is taxed at 45%, you're living pretty high on the hog.

45% on anything above £150k

Seriously? That seems way low.

The highest US bracket starts at $413k (for singles) or $464k (for joint filers) and is 39.6%.

The US and UK tax structures aren't THAT different. Only about 5% in the highest bracket. But our "highest bracket" starts substantially higher. And our Sales Tax is way lower. (I'm not sure how property taxes compare.)

-

Their taxes are incremental, like in the US. I don't know what their highest bracket is, but I assume if any portion of your income is taxed at 45%, you're living pretty high on the hog.

And one of the following will be true:

- Have found enough loopholes to pay effectively 0% tax

- Have not found #1, and will spend yourself into bankruptcy

- Hired an accountant to avoid #1 and #2, and will be embezzled into bankruptcy

-

The poor get super high deductible insurance that pays for nothing until they meet the high deductible they can't meet.

"Pays for nothing": One of the positive changes in Obamacare is the concept of a "minimum coverage", so every the cheapest plans now cover the essentials.

The theory on the cost was that the poor would form a risk pool (via the State or Federal insurance exchange) which would lower the cost over time. What wasn't compensated for is that the poor are generally a high-cost population and therefore pooling their risk doesn't help much, and also the Federal Exchange spent like 3 years being run by incompetent idiots.

(The lawmakers apparently did not understand that individuals who purchased coverage were already placed in a risk pool, so the cost they were paying was actually the normal cost for health insurance among that population.)

You made it worse for everyone, just to do nothing for the poor.

The ban on denying coverage based on pre-existing conditions is worth any missteps the rest of the legislation made.

My sister-in-law would never be able to be covered by non-work insurance plans because of her (successfully treated) cancer episode when she was a teenager. With Obamacare, she has gained job mobility she never had before-- meaning she can take more risks with her employment and make more money without losing her health-insurance coverage net. And she's just one of millions of people who have benefited.

That was HUGE.

And you want me to trust them with single payer?

On one hand, you have the Federal Government. On the other hand, you have a (practical) monopoly run by Blue Cross/Blue Shield. (Or Highmark, or whatever your local healthcare monopoly happens to be. They divvy up territory like a mafia.)

FUCK YEAH GIVE IT TO THE FEDS.

Oh another good point about Obamacare: it standardized procedure codes. So now you can directly compare costs between two different hospitals or clinics. Before, every hospital system had its own procedure codes, and every procedure code represented different things.

Anyway. Obamacare was definitely good legislation in many ways. Its biggest problem was that it was LARGE legislation. (The standardization of procedure codes could have been done separately from forming exchanges; as could have the ban on pre-existing coverage denials; as could have the concept of "minimum coverage".) So it's difficult to evaluate the effect of the whole package, and way too easy to find one bit of it you don't like (or that doesn't work) and call it a "failure" based on that.

The real problem in healthcare is the same problem we have in broadband Internet: domination by a few monopolies or effective-monopolies. Obamacare did nothing to weaken those monopolies, and in some ways made them larger. It also did nothing to make it easier to found a new health insurance company with less than a billion dollars of capital.

It's also done very little to de-incentivize unnecessary procedures. Doctors will call for an X-ray on an insured patient not because they need one to diagnose the patient, but because they get a little cha-ching back in their own pockets once the insurance company pays for it. In fact it creates a whole market in unnecessary medical scanners and technicians. Ironically, the big health insurance monopolies are starting their own initiatives to reduce unnecessary procedures, because it hits their pockets too.

Another problem in healthcare is that hospitals and clinics are incentivized into obscuring or flat-out lying about their prices, so they can charge a different rate to insurance providers than they charge to individuals off-the-street. Obamacare has done nothing about that and, again, possibly made it slightly worse by putting more people under the insurance umbrella.

So yes there are still a lot of problems. But at least Obamacare took on a few of the bigger ones, and more importantly: it actually brought the issue to into the daylight.

-

I agree with whatever @blakeyrat just said.

-

is the concept of a "minimum coverage", so every the cheapest plans now cover the essentials.

You enjoying paying for maternity coverage?

-

You enjoying paying for maternity coverage?

Yes. I am.

I also enjoy:

- Paying for public schools, even though I had no children who attend them

- Paying for roads and bridges I'll never drive on

- Paying for seaports in cities I'll never visit

- Paying for the Coast Guard to rescue migrants from countries I'll never go to to States I've never been to. And to bust drug runners, even though I don't do drugs

etc.

Look, that's all the shit that's already happening. It's just being done by a huge health insurance monopoly. Obamacare doesn't change that. If you were employed, you were in a risk pool and paying for neo-natal care before. If you were an individual, you were part of a risk pool and so were paying for neo-natal care before. THAT HAS NOT CHANGED.

The only possibly way you weren't paying for neo-natal before is if you were completely uninsured. Or I guess if you found a "men only" risk pool to belong to, but I'm 99.9% sure that never existed. (I can't speak for the entire industry, but our specific product hasn't even considered implementing something like that. We can do age bands, but not sex. Hell our system doesn't even store sex and gender separately.)

The question is whether you want those huge monopolies to be in charge of the process, or whether you want the Government to have a bigger say in it. Like I said above, I'd prefer the Feds over Premera Blue Cross. ANY FUCKING DAY OF THE WEEK.

-

Their taxes are incremental, like in the US. I don't know what their highest bracket is, but I assume if any portion of your income is taxed at 45%, you're living pretty high on the hog.

People keep missing my point.

Income tax is only half the tax you pay.

If you're at tax bracket 25%, you're paying half your income in total taxes from all source to the government.

The total taxes the richest pay would be 75%, if they didn't have loopholes.

The ban on denying coverage based on pre-existing conditions is worth any missteps the rest of the legislation made.

That's debatable, because it places emotional arguments based on specific instances, and does not consider the net effect. Besides, like I said before. People made this sound like it could affect anyone, but even if you changed carrier due to changing jobs, the existing law protected. Which left people like you said, teenagers that were still tied to their parents insurance or lack of insurance.

But that's besides the point. The points of the bill that actually do the most harm aren't related to preexisting conditions, but rather the relationship between insurance and individuals.

The trickle down cost of higher risk people having their risk tied to their age not being able to demand more premium, is what's making the premiums the most.

On one hand, you have the Federal Government. On the other hand, you have a (practical) monopoly run by Blue Cross/Blue Shield. (Or Highmark, or whatever your local healthcare monopoly happens to be.)

FUCK YEAH GIVE IT TO THE FEDS.

I love that one.

"The businesses are monopolies. But singer payer government isn't a monopoly"

At which point I hear.

"But the government doesn't make profit."

The net profit of companies is relatively small, and the government still has its bottom line.

The per premium payer declined coverage was the same % for Medicare and other government coverage as private coverage prior to the law change, so the government hasn't performed any better in coverage than the private corporations.

So it's difficult to evaluate the effect of the whole package, and way too easy to find one bit of it you don't like (or that doesn't work) and call it a "failure" based on that.

##I will agree, there are several good parts of the law.

However, it's just as easy to find one bit you do like, and call it a "success" based on that.

I wouldn't call it a failure, it's doing exactly what it proposed to do. It's just that what the politicians said it would do and what the law was written to do are two different things.

When Obama said you could keep your current plan, that was outright a lie. There was no grandfather clause for existing plans, and plans had to meet new requirements. Almost certainly increasing the baseline coverage alone increased the premiums.

But what it did do was equalize the premiums based on age. That's why healthy middle aged are seeing as much as a magnitude higher in premiums, and the elderly are seeing their coverage cut in half.

Again, most of the benefit went to the insurance companies themselves. It says something when the politicians are railing on the evil private insurance companies, and at the same time insurance companies were for the law.

The real problem in healthcare is the same problem we have in broadband Internet: domination by a few monopolies or effective-monopolies.

I would say there are bigger problems with actual healthcare cost, the level of frivolous lawsuits, and the fact that insurance companies make doctors give a discount, and then don't always actually pay doctors the portion they tell you they are paying.

From insider knowledge, after a discount insurance will claim to cover the remaining 80%, and you'll pay 20%, but then insurance won't actually pay the full 80%. Medical field has to fight insurance to actually pay that amount, which drives up costs.

Insurance companies also, sometimes, mandate what medical places have to charge for out of network, to compensate for the deals they give to in-network. And of course, for those instances, the insurance company pays little to nothing.

Another problem in healthcare is that hospitals and clinics are incentivized into obscuring or flat-out lying about their prices, so they can charge a different rate to insurance providers than they charge to individuals off-the-street. Obamacare has done nothing about that and, again, possibly made it slightly worse by putting more people under the insurance umbrella.

Well, I guess I wasted time on my last point, you made it for me. Yes, this is a major problem.

But at least Obamacare took on a few of the bigger ones,

Actually it didn't take on any of the major issues, outside of pre-existing conditions.

It simply redistributed the costs, and made some risk categories non-applicable.

The insurance company to premium holder relationship isn't the problem. The AHA is a band-aid at best, and it's a band-aid that will burst in the next decade, and we'll have a bigger problem later.

We are bleeding cancer here. A band-aide isn't going to help.

. If you were an individual, you were part of a risk pool and so were paying for neo-natal care before. THAT HAS NOT CHANGED.

No, the only thing that changed is that the insurance companies made it visible so they could charge 2 to 3 times more than they did before.

My beef is that the bulk of premium payers had their coverage raised by a inordinate amount greater than the extra coverage being provided to other risk categories.

-

teenagers that were still tied to their parents insurance or lack of insurance

/me waves hand

Filed Under: Type I diabetes sucks

-

Have you seen what passes for employer plans these days?

We got a new CEO and and they upped the company contribution and the deductible went down by about $500. I was pretty shocked.

-

Yes, I know.

That's why I'm totally ok with the pre-existing coverage ban thing.

I WILL pay for that.

-

Imo "The biggest problem" in both the Eu and us is lobbyism. They bias the politics too far towards big companies.

Which is a thing because the government has set itself up with so much power and money.

-

I was pretty shocked.

Yeah, the good companies, with all their evil profit, are doing a bang up job insulating the middle-class. And they have no motivation to do so.

It's almost like.... they care....

I don't know what to think.

-

Which is a thing because the government has set itself up with so much power and money.

Yeah, I've been trying to get companies to lobby to charities, or third world countries.

-

Oh another good point about Obamacare: it standardized procedure codes. So now you can directly compare costs between two different hospitals or clinics. Before, every hospital system had its own procedure codes, and every procedure code represented different things.

Huh? Those have been standard for a long time. I used to do health care billing about 20 years ago and it was all standardized. The codes just updated this year (and all of my doctors have been bitching about this).

-

Wow....

Half your income....

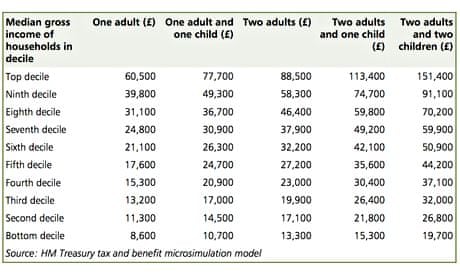

Remembered I had this lying around from a post I made elsewhere. Applicable for the 2014/2015 tax year as I recall:

Across the bottom is the gross wage.

Blue: IT: Income Tax

Orange: NI: (Employee's) National Insurance

Yellow: Eployer's NI: The bit that doesn't appear on your pay slip.Note that the final absolute percentages here are lower than the numbers talked about above because this chart includes the default nil-rate bands.(e.g. £8,113 before NI starts getting charged, £10,600 before income tax kicks in.)

The percentages mentioned previously are the marginal rates (i.e. having already earned and been taxed on £15,000, how much of your next £100 gets taxed...?)

For a rough estimate, decile wages from 2014 (latest I could easily find.)

-

That's debatable, because it places emotional arguments based on specific instances, and does not consider the net effect.

Ok.

Besides, like I said before. People made this sound like it could affect anyone, but even if you changed carrier due to changing jobs, the existing law protected.

In theory, yes. In reality, if the new employer lays you off 6 months down the line you're completely fucked with no insurance and no way to buy insurance. Which means people with pre-existing conditions had an strange unnatural pressure to keep their existing job and not "make waves" by asking for raises too often.

Which left people like you said, teenagers that were still tied to their parents insurance or lack of insurance.

She had cancer when she was a teenager. It was cured at the time, on her parents' insurance. Despite that, before Obamacare, that had PROHIBITED HER FROM EVER PURCHASING INDIVIDUAL HEALTHCARE COVERAGE FOR THE REST OF HER ENTIRE LIFE. EVER.

Do you think that was fair or just?

The trickle down cost of higher risk people having their risk tied to their age not being able to demand more premium, is what's making the premiums the most.

Right; but you're also forgetting how grossly inefficient the entire system is. There's a SHITLOAD of fat to trim before we should get to the point of worrying about that.

I love that one.

"The businesses are monopolies. But singer payer government isn't a monopoly"

It is a monopoly. I never said otherwise. The word "monopoly" isn't a synonym for "awful demon hell evil Hitler++".

But it has WAY different incentives than Blue Cross/Blue Shield does. That's the key. Specifically, Blue Cross/Blue Shield is incentivized to keep health insurance inefficient and expensive. (Why are those "trickle down" premiums you're so concerned about going up? Think about what market factors are causing that.) The Federal Government would have the opposite incentive.

At which point I hear.

"But the government doesn't make profit."

The US Post Office is part of the Federal Government, but makes a profit. Most of the time.

The net profit of companies is relatively small, and the government still has its bottom line.

You are high as fuck if you believe this is true. Blue Cross/Blue Shield are making "relatively small" profits? Jesus. The Feds had to cap how much they skim off the top of procedures, and they're STILL pulling in billions.

The per premium payer declined coverage was the same % for Medicare and other government coverage as private coverage prior to the law change, so the government hasn't performed any better in coverage than the private corporations.

The government has no influence (except a very rough one-- basically a binary "accept or do not accept") over providers.

Standardizing procedure codes is a small first step in that direction.

I wouldn't call it a failure, it's doing exactly what it proposed to do. It's just that what the politicians said it would do and what the law was written to do are two different things.

That goes back to my criticism of it being too large.

When Obama said you could keep your current plan, that was outright a lie.

He said that about people who were employed, and it was mostly true. I don't think anybody employed had a plan that would have had to change to meet minimum coverage requirements.

But what it did do was equalize the premiums based on age. That's why healthy middle aged are seeing as much as a magnitude higher in premiums, and the elderly are seeing their coverage cut in half.

Right; and if I had written it, I'd have lowered the age of Medicare eligibility. Possibly sliding, so each year the eligibility goes down by two years. Until Medicare becomes the US' single-payer solution. Simple and easy.

I'm not sure why the Democrats didn't do that.

Again, most of the benefit went to the insurance companies themselves.

They have the most lobbyists. Despite your weird assertion that they make hardly any profit, huh!

It says something when the politicians are railing on the evil private insurance companies, and at the same time insurance companies were for the law.

The insurance monopolies were not for the law originally. That changed. For most of them it didn't change until it was obvious the law would be passed regardless.

I would say there are bigger problems with actual healthcare cost, the level of frivolous lawsuits,

That's also a factor. There are many factors.

and the fact that insurance companies make doctors give a discount, and then don't always actually pay doctors the portion they tell you they are paying.

And yet doctors aren't generally seen in the food bank grabbing cans of expired-in-1995 beets, hmmmm. Poor babies.

Medical field has to fight insurance to actually pay that amount, which drives up costs.

This overhead of price bickering is also a factor. There are many factors.

Actually it didn't take on any of the major issues, outside of pre-existing conditions.

You don't think standardizing procedure codes, or enforcing a minimum standard of coverage were good? Or maybe you don't think they were "major issues"? I disagree utterly.

The insurance company to premium holder relationship isn't the problem. The AHA is a band-aid at best, and it's a band-aid that will burst in the next decade, and we'll have a bigger problem later.

I don't think anybody's denying that Obamacare is a temporary solution, Obama even flat-out said that when he was promoting the legislation. It's not the permanent fix.

No, the only thing that changed is that the insurance companies made it visible so they could charge 2 to 3 times more than they did before.

But they aren't make any profit! Those poor Blue Cross/Blue Shield CEOs, out begging on the streets! Poor babies. Awww.

My beef is that the bulk of premium payers had their coverage raised by a inordinate amount greater than the extra coverage being provided to other risk categories.

That's not true. The bulk of individuals perhaps. Those with employer-provided insurance (the vast majority of Americans) have also seen a rise, but not one out-of-line with pre-Obamacase rises. The rates have been going up for decades, it didn't start when Obama got into office.

-

"You pay only 1/4 your wages in income tax" is true.

But that's not the only taxes you pay.

-

Huh? Those have been standard for a long time. I used to do health care billing about 20 years ago and it was all standardized. The codes just updated this year (and all of my doctors have been bitching about this).

My understanding was that only codes for procedures covered by Medicare were standardized previously.

But maybe I'm wrong.

-

With any luck, that number is just going to increase.

-

In theory, yes. In reality, if the new employer lays you off 6 months down the line you're completely fucked with no insurance and no way to buy insurance.

I thought we had gap coverage for unemployment.

Of course, you still had to pay the premium, which might be hard given now you had to pay the full amount, but you also got unemployment pay.

Yeah, it sucks.

Of course, there are a multitude of reasons not to rock the boat, I don't earn enough to go a year without pay either.

But this did put higher pressure on these people.

Do you think that was fair or just?

No, which is why I've said repeatedly, I'll pay for protecting people from pre-existing condition coverage. It's a relatively small portion, so it has less impact.

Right; but you're also forgetting how grossly inefficient the entire system is. There's a SHITLOAD of fat to trim before we should get to the point of worrying about that.

That is the biggest multiplier there is. End term coverage is 80 - 99% of the coverage you'll need. And it accounts for 10% of your life expectancy.

Specifically, Blue Cross/Blue Shield is incentivized to keep health insurance inefficient and expensive.

I disagree with the inefficient part.

The Federal Government would have the opposite incentive.

But in practice, they turn out the same decline % of coverage.

###Either they are lying about their incentives, or they are grossly incompetent.

The US Post Office is part of the Federal Government, but makes a profit. Most of the time

Not sure what to believe here. I get just as many sources saying they are losing money.

That goes back to my criticism of it being too large.

The reason almost doesn't matter.

I believe that they knew what it was going to do, and flat out lied about it.

If not, then they are also grossly incompetent at reading the law.

I don't think anybody employed had a plan that would have had to change to meet minimum coverage requirements.

Other than 20% - %100 increase in premiums.

Right; and if I had written it, I'd have lowered the age of Medicare eligibility. Possibly sliding, so each year the eligibility goes down by two years. Until Medicare becomes the US' single-payer solution. Simple and easy.

You have to solve the donut hole first. And, yes, they did the exact opposite of this. They actually reduced Medicare. Another reason insurance companies liked the law. Also, another point on the board for either the grossly incompetent, or the lying team.

If I put on my tin foil hat here, I'd have to believe that the Democrats had relationships with insurance companies that rival the Republicans relationships with oil companies.

They have the most lobbyists. Despite your weird assertion that they make hardly any profit, huh!

No, no. They make lots of profit. It's just that the net profit to expenditure % is much lower than people think. And that making it single payer based on "they make profit" alone will have little benefit.

Most likely, the government will outsource the insurance to private no matter what. Adding another layer of costs, increasing the premiums even higher. So their single payer solution will baseline be higher in cost for the overhead alone. If they manage to restrict net profit, they might balance it out. Leaving the population to say, "we have single payer", while not really doing anything in reality.

Our government isn't the type to want to be the payer for insurance.

That's why they keep reducing medicare.

And yet doctors aren't generally seen in the food bank grabbing cans of expired-in-1995 beets, hmmmm. Poor babies.

Actually most doctors were arguing because they felt that the changes in coverage would reduce the amount of care they would be able to give based on insurance coverage.

I do not know why they believed that, to be honest. I would have to investigate.

You don't think standardizing procedure codes

That seems to be a redundant effort. The prices for out-of-network coverage were standardized. Insurance companies told doctors what to charge for out-of-network coverage. If it wasn't standard then there would have been a lot of confusion.

Maybe it wasn't standard to the premium payer, but it was standard in some level.

enforcing a minimum standard of coverage were good

Actually no.

That has little to no effect. It simply wiped a level of coverage off the table.

Same effect as raising the minimum wage. It simply wipes a level of job off the table.

I would have rather they made standardized brackets, and subsidized the poor up to the standard they found to be acceptable. Leaving middle class the option to choose their coverage level.

But they aren't make any profit! Those poor Blue Cross/Blue Shield CEOs, out begging on the streets! Poor babies. Awww.

I'm going to go the Democrat way of saying "they're too big to fail" by pointing out that the company has more than just a CEO. There are jobs at stake.

but not one out-of-line with pre-Obamacase rises.

Some report as much as 2-3x increase. That is out of line.

And for many, the increase was hidden behind increasing deductibles that went up as much as 2-10x.

-

Speaking of American health care debates, did you know my GoFundMe is still running?

-

In reality, if the new employer lays you off 6 months down the line you're completely fucked with no insurance and no way to buy insurance.

Oh, look who's never heard of COBRA.

-

Oh, look who's never heard of COBRA.

Like I said, he's going to point out that you no longer have the employer's portion of the premium and that you have reduced income from unemployment payments.

But at least you pay no taxes for the duration.

Much of the law was redundant with existing protections, but managed to accomplish the same with increasing levels of inefficiency.

-

Either they are lying about their incentives, or they are grossly incompetent.

:whynotboth.wav:

again...

again...{kind=link}