401(k) Plans No Longer Make Much Sense for Savers

-

-

The employer contribution is still valuable, with a 100% match worth 2.3% per year in extra return over 30 years, but this has nothing to do with the 401(k) structure.

This is not something that should be ignored in the discussion, though. Every employer I've ever had did some matching. I totally agree with 0% matching a 401(k) makes no sense, but let's be honest, how many employers don't offer it? I know if during a job interview they mentioned they offer a 401(k) but don't match, I'd laugh in their face and leave.

-

@The_Quiet_One But like if 401k doesn't make any sense, wouldn't you rather get those 2% or whatever in your paycheck?

-

The marginal federal income tax rate was 43% in 1980, 12% today

Yeah, but contributing to a traditional account reduces the amount I'm putting into the highest bucket. Every dollar I put in saves me $0.24 now, and likely in the near future $0.32/dollar

But otherwise, yes. 401(k)s need to provide more of a benefit for workers in the lower tax brackets.

-

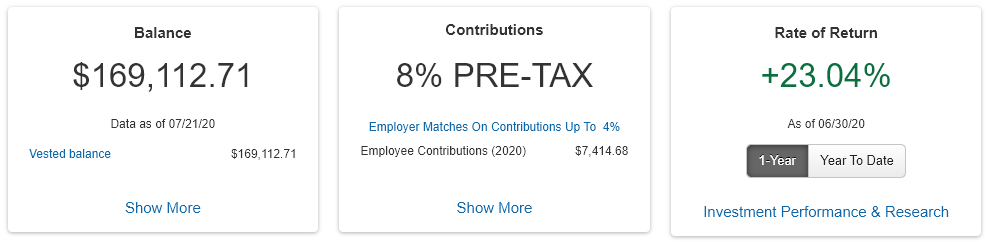

Seems like it's doing OK for me.

-

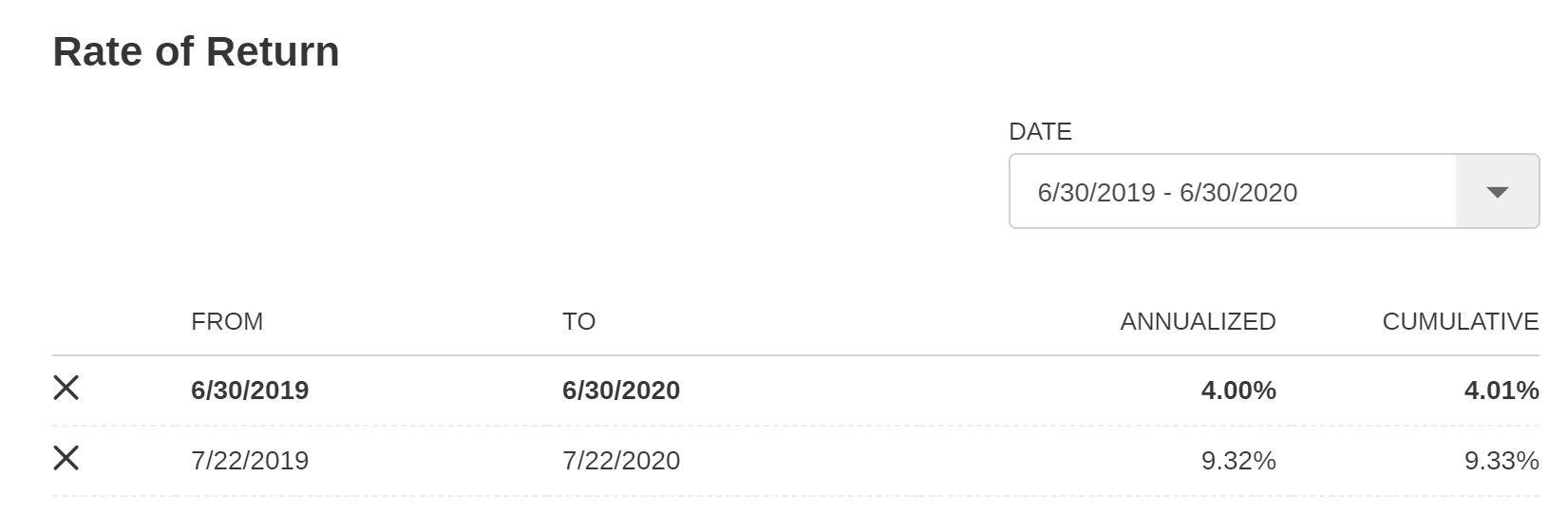

@error That looks good, although there's been a lot of volatility recently. My numbers for that same period as you look pitiful, but the 1-year return looking back from today instead of 6/30 isn't bad:

Anyways: as a single person making non-crap amounts of money, the tax benefits are still there. Maybe if you're married and don't get an employer match and your 401(k) vendor has terrible fees (I pay 0.02% in fees + a 0.06% expense ratio on the target date fund - a far cry from their "1-2%"), avoiding the 401(k) might make sense. But that seems like an unusual case.

-

@The_Quiet_One said in 401(k) Plans No Longer Make Much Sense for Savers:

This is not something that should be ignored in the discussion, though. Every employer I've ever had did some matching. I totally agree with 0% matching a 401(k) makes no sense, but let's be honest, how many employers don't offer it? I know if during a job interview they mentioned they offer a 401(k) but don't match, I'd laugh in their face and leave.

This -- matching is mandatory in a 401(k) or similar (like SIMPLE IRA), and it's simply compensation you're not taking. You'd be better off taking the match, then withdrawing the money pre-retirement (penalties and all) than not taking it at all.

As the article may point out, the main benefit of the 401(k) is to offer highly-compensated individuals a relatively easy way to do tax-differed retirement savings. If you don't do this, then they will simply find another way (a "loophole" so to say), which will then have to be "patched" later. The secondary benefit is to provide management feeds to accounting/management companies that oversee the 401(k) plan. They aren't cheap to run.

Personally, I think the ROTH-IRA (post-tax savings) is a significantly better scheme than pre-tax savings, if for no other reason that it serves as a much better savings scheme. Dump as much as you can/want into your ROTH, and you aren't penalized if you take if it out because you put too much in.

-

One easy change is to allow workers to roll 401(k) funds over to self-directed IRAs at any time (now they can do it only when they leave a job). 2 That would force 401(k) platforms to compete in an open market, and it costs nothing.

That seems like a no brainer. What was the rationale for restricting it in the first place? Fund companies wanted it?

-

@apapadimoulis said in 401(k) Plans No Longer Make Much Sense for Savers:

Personally, I think the ROTH-IRA (post-tax savings) is a significantly better scheme than pre-tax savings, if for no other reason that it serves as a much better savings scheme. Dump as much as you can/want into your ROTH, and you aren't penalized if you take if it out because you put too much in.

My RWNJ paranoia kicks in whenever I read about these things. I just don't trust that they won't come back and re-tax them eventually.

-

@apapadimoulis said in 401(k) Plans No Longer Make Much Sense for Savers:

Personally, I think the ROTH-IRA (post-tax savings) is a significantly better scheme than pre-tax savings, if for no other reason that it serves as a much better savings scheme. Dump as much as you can/want into your ROTH, and you aren't penalized if you take if it out because you put too much in.

From a purely self-interest perspective, standard (tax-deferred) IRA makes sense if the taxes you'll be paying upon withdrawal will be lower than today's rate, while Roth makes sense if they would be higher. Considering that income taxes are at a historically low level right now, and that societal attitudes towards such matters tends to oscillate on an 80ish-year cycle, IMO it makes very little sense for anyone working today, with the possible exception of those who are imminently approaching retirement age, to use a standard IRA.

-

Lack of matching seems to be common here, as if I needed more proof that my state is a third world country.

So last year, after decades of attacking constitutionally protected pensions, the state finally broke the pension plan for new hires. New hires get two choices - a hybrid 401k/pension plan or just the 401k. The 401k is all sorts of fraudulent. It's all of the bad parts of a pension with none of the good. First, employee contribution is mandatory. Second, employees have no option to self direct any portion. Third, nobody believes the match will survive long, after 11 years of the state not making its much more strictly required contributions to the pension fund (thus the current "crisis").

If I was going to save on my own, it'd be an IRA with my credit union. Unfortunately, they talked me out of opening one for some reason several months ago. That's fine. I've tripled my money in stocks by myself. Problem is I didn't have much to triple. I think once I get out from under business debt, which I'm on track to do by the end of 2021, I'll be able to bank way more money on a consistent basis, even if it's into a regular savings account.

-

@dangeRuss said in 401(k) Plans No Longer Make Much Sense for Savers:

Discuss

Ha! Not falling for that one again.

-

@dangeRuss said in 401(k) Plans No Longer Make Much Sense for Savers:

@The_Quiet_One But like if 401k doesn't make any sense, wouldn't you rather get those 2% or whatever in your paycheck?

Do you know what matching is?

-

@The_Quiet_One said in 401(k) Plans No Longer Make Much Sense for Savers:

@dangeRuss said in 401(k) Plans No Longer Make Much Sense for Savers:

@The_Quiet_One But like if 401k doesn't make any sense, wouldn't you rather get those 2% or whatever in your paycheck?

Do you know what matching is?

I think he's saying that instead of doing a "matching" contribution for them to just give you that in your salary. Of course, you'd have to take out their payroll tax portion on that (which isn't that big, but still).

-

@boomzilla said in 401(k) Plans No Longer Make Much Sense for Savers:

@The_Quiet_One said in 401(k) Plans No Longer Make Much Sense for Savers:

@dangeRuss said in 401(k) Plans No Longer Make Much Sense for Savers:

@The_Quiet_One But like if 401k doesn't make any sense, wouldn't you rather get those 2% or whatever in your paycheck?

Do you know what matching is?

I think he's saying that instead of doing a "matching" contribution for them to just give you that in your salary. Of course, you'd have to take out their payroll tax portion on that (which isn't that big, but still).

That doesn't really work, though. The whole point of the contribution is that it matches what you're already willing to put aside for retirement. The employer is giving me 5% of my salary because I'm willing to reduce my immediate salary by 5%. My colleague might not be participating in the 401(k) at all, so she gets 0%. Other colleague might be doing 3%... if they suddenly remove the 401(k) plans, who gets what? It seems arbitrary to me, and in the end makes no sense because the whole point of the matching contribution is it's based on what the employee elects to do.

The same employer who is "generously" matching the 401(k) is necessarily going to just give that money away without a 401(k) because the contribution is a value added to a benefit. It's no different than if you expect an employer to just give everyone whatever they're contributing to each employee's health insurance premiums in lieu of an employer-provided health insurance plan. Everyone's premiums are different based on their marital and family status, and what plan they sign up for, among other things, so how do you define how much equivalent salary they are entitled to without that benefit in place?

-

@The_Quiet_One yes, I agree, the proposal is overly simplistic and not realistic.

-

@boomzilla said in 401(k) Plans No Longer Make Much Sense for Savers:

My RWNJ paranoia kicks in whenever I read about these things. I just don't trust that they won't come back and re-tax them eventually.

They could, but I think that'd be tantamount to a new tax (wealth tax?), which could happen anytime. "They" could also just confiscate all of your savings as tax, so really your only "safe" bet is gold boolean .

@Mason_Wheeler said in 401(k) Plans No Longer Make Much Sense for Savers:

From a purely self-interest perspective, standard (tax-deferred) IRA makes sense if the taxes you'll be paying upon withdrawal will be lower than today's rate, while Roth makes sense if they would be higher. Considering that income taxes are at a historically low level right now, and that societal attitudes towards such matters tends to oscillate on an 80ish-year cycle, IMO it makes very little sense for anyone working today, with the possible exception of those who are imminently approaching retirement age, to use a standard IRA.

This makes sense, and I've learned from financial advisors that "wealth management" is a lot about emotional management. Purely financially speaking, your'e right. But I don't think it makes a big difference either way, at least compared to your contribution and other financial habits.

The standard IRA might be better for someone who needs a huge barrier to prematurely withdrawing those funds (i.e. "I need an emergency vacation to Disneyland"), and the Roth IRA is better for someone who is terrified of locking up money (i.e. better save just in case I need an emergency heart transplant and i forget to renew y insurance).

-

@Mason_Wheeler said in 401(k) Plans No Longer Make Much Sense for Savers:

From a purely self-interest perspective, standard (tax-deferred) IRA makes sense if the taxes you'll be paying upon withdrawal will be lower than today's rate, while Roth makes sense if they would be higher. Considering that income taxes are at a historically low level right now, and that societal attitudes towards such matters tends to oscillate on an 80ish-year cycle, IMO it makes very little sense for anyone working today, with the possible exception of those who are imminently approaching retirement age, to use a standard IRA.

You're overlooking that US tax brackets are progressive.

If I put away my money in a Roth account, it comes "off the top", and I'd have to pay 24% tax on it now. If I put it into a standard account, it seems... unlikely... that the minimum tax bracket is going to be >= 24% in the future.

More specifically, I took a look at the tax brackets from 1950, 1960, 1970, and 1980. I may have bungled the math, but it looks like even with the "worst case" numbers adjusted for inflation to 2020 dollars - 1980 specifically - I'd still have $53K of income (plus the standard deduction) that would be taxed at a rate below what I'd pay if I put it in a Roth today.

(Personally, I hedge my bets - standard 401(k) and Roth IRA. If/when I start making too much for a Roth IRA, I'll have to reconsider.)

@apapadimoulis said in 401(k) Plans No Longer Make Much Sense for Savers:

They could, but I think that'd be tantamount to a new tax (wealth tax?), which could happen anytime.

Depends on how/what was done. Saying "Roth IRA gains are no longer exempt from capital gains tax", treating them like any other investment account, might fly under the radar as not being a "new" tax.

-

@apapadimoulis said in 401(k) Plans No Longer Make Much Sense for Savers:

so really your only "safe" bet is gold boolean

Isn't it already illegal to own gold in US?

-

@Gąska nope! In fact, you can buy bullion directly from the US Mint if you want. I know there's some history that made it illegal for a bit, and then there was some stuff with Krugerrands that made the plot of movies, but if you really wanna capture your wealth in chunks of precious metal, by all means.

-

Another advantage of a 401(k) is that the barrier to entry is "one of those forms you filled out when you started your job" and the ongoing attention needed is "Here's that report they send me every year." Any saving is good, matched saving is better, and saving you don't have to think about is great.

-

@Parody that said, not thinking is a suboptimal saving strategy.

-

So, who's on first?

@apapadimoulis said in 401(k) Plans No Longer Make Much Sense for Savers:

The standard IRA [...] Roth IRA

I'm not clear how they fit in relation with the Official, Provisional or Real IRAs?

@apapadimoulis said in 401(k) Plans No Longer Make Much Sense for Savers:

bullion directly from the US Mint

Mint bouillon

-

@apapadimoulis said in 401(k) Plans No Longer Make Much Sense for Savers:

@boomzilla said in 401(k) Plans No Longer Make Much Sense for Savers:

My RWNJ paranoia kicks in whenever I read about these things. I just don't trust that they won't come back and re-tax them eventually.

They could, but I think that'd be tantamount to a new tax (wealth tax?), which could happen anytime. "They" could also just confiscate all of your savings as tax, so really your only "safe" bet is gold boolean .

No, this would just be a new capital gains tax. Not the same as a wealth tax, just repealing a promise not to tax that income. In theory a state could make a wealth tax but I don't see that happening. It's not completely impossible for the Feds to do that, but there are some significant Constitutional hurdles (but of course the right Justicies and Bob's your taxman).

-

@Gąska said in 401(k) Plans No Longer Make Much Sense for Savers:

@Parody that said, not thinking is a suboptimal saving strategy.

But unthinkingly saving is far superior to just about any kind of not saving (exceptional circumstances excepted).

-

@boomzilla In other words, having money is better than not having money

-

@remi said in 401(k) Plans No Longer Make Much Sense for Savers:

@boomzilla In other words, having money is better than not having money

Yes, but in the future.

-

@boomzilla

:wow_that_s_deep_man:

-

-

Coming up next!

:@remi::

:obama_not_bad:

:

: :mission_accomplished:

:@remi:: the emoji thread is

: PR accepted.

:@everyone else:: fuck off/get a room!etc.

-

@Gąska said in 401(k) Plans No Longer Make Much Sense for Savers:

@Parody that said, not thinking is a suboptimal saving strategy.

It's a better strategy than

.

.I mean, they're both

, but one is with savings and the other is with no savings.Edit:

-

@Unperverted-Vixen said in 401(k) Plans No Longer Make Much Sense for Savers:

If/when I start making too much for a Roth IRA, I'll have to reconsider.

Since the limit is $132,000 (I'm single), and I work in Silly Valley, that ship sailed a long time ago...

I just had the fun of discovering that my current company does the 401K catch up amount differently (it's a company 401 instead of being managed by someone like Fidelity). In the past, I just set my withholding percentage, and base+catchup (19500+6500 for 2020) went into the 401. Here, the percentage only applies to the base amount. So I was surprised to see the last paycheck max at 19500 and the leftover be applied as after-tax. (First though: WTF? That's too early...) Several phone calls later to payroll/retirement people (we do actually have a good help system!) I discovered I have to actually sign up for the catchup amount.

Maybe next year things will actually be right... (last year, they ignored my withholding at my previous company, so I almost got into tax trouble because of too much going into the 401. Corrected W2s are a pain.)

-

@The_Quiet_One said in 401(k) Plans No Longer Make Much Sense for Savers:

It's no different than if you expect an employer to just give everyone whatever they're contributing to each employee's health insurance premiums in lieu of an employer-provided health insurance plan. Everyone's premiums are different based on their marital and family status, and what plan they sign up for, among other things, so how do you define how much equivalent salary they are entitled to without that benefit in place?

My wife's old company had a medical insurance buy-out, which was great and helped pay for things, but we only did it for a year before she switched jobs.

-

@apapadimoulis said in 401(k) Plans No Longer Make Much Sense for Savers:

The standard IRA might be better for someone who needs a huge barrier to prematurely withdrawing those funds (i.e. "I need an emergency vacation to Disneyland"), and the Roth IRA is better for someone who is terrified of locking up money (i.e. better save just in case I need an emergency heart transplant and i forget to renew y insurance).

Don't forget those who can't get a deduction for contributing to the standard IRA because of income raising and have to backdoor Roth anyway.

-

@apapadimoulis said in 401(k) Plans No Longer Make Much Sense for Savers:

As the article may point out, the main benefit of the 401(k) is to offer highly-compensated individuals a relatively easy way to do tax-differed retirement savings. If you don't do this, then they will simply find another way (a "loophole" so to say), which will then have to be "patched" later.

Uhmmmmm, sort of. As long as they aren't too highly compensated. I think the income ceiling is ~$140,000 if you're single and ~$200,000 for married filing jointly.

-

@Polygeekery From a quick glance at US household income distribution, $200k is about the 95% percentile (2014 numbers but the ballpark figure is unlikely to be hugely different now).

So yeah, I would say that it's firmly in the "highly-compensated" territory.

That it doesn't seem so to you might be telling about your own income...

-

@remi said in 401(k) Plans No Longer Make Much Sense for Savers:

That it doesn't seem so to you might be telling about your own income...

Well, not really. Considering that we are on a technology forum based out of the USA there is likely a fair number of people that this affects. Also, I never said that it would not be highly compensated. I said:

@Polygeekery said in 401(k) Plans No Longer Make Much Sense for Savers:

As long as they aren't too highly compensated.

-

@Polygeekery said in 401(k) Plans No Longer Make Much Sense for Savers:

Considering that we are on a technology forum based out of the USA there is likely a fair number of people that this affects.

Again, a quick search tells me that "computer programmers" (whatever that means) have a median income of $86k, which is significantly higher than the overall median of $62k. Still, the same page puts the 90% percentile at $140k whereas Wiki puts it at $160k overall, so... I'm not really sure how different the income distribution of this forum is compared to the overall US one... it's likely skewed towards higher salaries, for sure, but to what degree... ?

Anyway, that's just pointless

ing.

ing.

-

@remi however, if you're in a high cost of living area (Silly Valley, NYC, etc) it's not crazy to have a $100K+ income. And if you're married, odds are that your spouse works, too, so again, not crazy to have $200K+ dual incomes in those places.

-

@boomzilla said in 401(k) Plans No Longer Make Much Sense for Savers:

however, if you're in a high cost of living area (Silly Valley, NYC, etc) it's not crazy to have a $100K+ income

That's starting salary for newbies. (hell, I was making that much 20+ years ago with only 5yrs experience at the time)

edit: Forgot to mention - remember that 100K is considered "low-income" here. (first googled article - from 2018)

-

@boomzilla Yes, yes, I know... If you live there, if you're not grossly underpaid, if your spouse is making the same as you do, if...

I'm not saying those incomes don't exist, they obviously do. But if they were that common, they would be visible in pretty much any income distribution, whichever way you slice it (by state, by employment...). From the quick searches I made, they're not. $200k per household (or $100k per individual) is, whichever way you look at it, very likely in the higher reaches of employment, even if you restrict yourself to the US population of this forum.

-

@remi said in 401(k) Plans No Longer Make Much Sense for Savers:

I'm not saying those incomes don't exist, they obviously do. But if they were that common, they would be visible in pretty much any income distribution, whichever way you slice it (by state, by employment...). From the quick searches I made, they're not. $200k per household (or $100k per individual) is, whichever way you look at it, very likely in the higher reaches of employment, even if you restrict yourself to the US population of this forum.

This thread is a roller coaster for my self-esteem about my salary.

-

@boomzilla said in 401(k) Plans No Longer Make Much Sense for Savers:

@Gąska said in 401(k) Plans No Longer Make Much Sense for Savers:

@Parody that said, not thinking is a suboptimal saving strategy.

But unthinkingly saving is far superior to just about any kind of not saving (exceptional circumstances excepted).

And if there's anyone good at not saving, it's the people of the good ol' U S of A!

WOO!

-

@Unperverted-Vixen said in 401(k) Plans No Longer Make Much Sense for Savers:

You're overlooking that US tax brackets are progressive.

If I put away my money in a Roth account, it comes "off the top", and I'd have to pay 24% tax on it now. If I put it into a standard account, it seems... unlikely... that the minimum tax bracket is going to be >= 24% in the future.

That's not quite right: Roth accounts are after-tax dollars, so you're paying your average tax on that money. It's the non-Roth accounts that use the "off the top" money, because they reduce your taxable amount. If you're single making $80k (or married $160k), the average tax rate is around 15%, even though your marginal rate is 22%.

@apapadimoulis said in 401(k) Plans No Longer Make Much Sense for Savers:

They could, but I think that'd be tantamount to a new tax (wealth tax?), which could happen anytime.

Depends on how/what was done. Saying "Roth IRA gains are no longer exempt from capital gains tax", treating them like any other investment account, might fly under the radar as not being a "new" tax.

Eh, I think you'd get a lot of screaming bloody murder if that happened. Opponents would have easy ammunition with "taking money from retirees," and old people vote more than young people, so there'd be some pretty solid resistance. It wouldn't be (quite) as noisy as a New Tax, but you'd certainly hear about it before it happened. And then, of course, you

contact your representativewhine on a forum or two and call it a day..

-

@PotatoEngineer said in 401(k) Plans No Longer Make Much Sense for Savers:

That's not quite right: Roth accounts are after-tax dollars, so you're paying your average tax on that money.

They are after-tax dollars, but I'm not paying my average tax rate on them. As you said, if you switch from post-tax to pre-tax it comes out of that top tax bracket. But the reverse happens when you go from pre-tax to post-tax. It's always based on your highest bracket(s), not the average.

-

@Unperverted-Vixen said in 401(k) Plans No Longer Make Much Sense for Savers:

@PotatoEngineer said in 401(k) Plans No Longer Make Much Sense for Savers:

That's not quite right: Roth accounts are after-tax dollars, so you're paying your average tax on that money.

They are after-tax dollars, but I'm not paying my average tax rate on them. As you said, if you switch from post-tax to pre-tax it comes out of that top tax bracket. But the reverse happens when you go from pre-tax to post-tax. It's always based on your highest bracket(s), not the average.

I'm afraid I disagree with you; if you're putting after-tax dollars anywhere, they've been taxed at your average. There's no way to say whether the money came from the first bracket or the last bracket. The money you pay on rent and the money you put in your Roth IRA both come from the same pool of money (i.e., all post-tax money), so they've been taxed at the average of all of your post-tax money.

But for pre-tax dollars, your adjusted income is decreased by one dollar for every dollar you put in the 401(k)-or-equivalent. That decrease-by-one-dollar bit means that it must be affecting money that's in the highest tax bracket, because all of the lower brackets are unaffected. Earning $1000 less doesn't change the taxes you paid in the second bracket (

unless your maximum bracket was the second bracket, of course).I guess I'm not quite following you when you talk about changing from post-tax to pre-tax and vice versa; I'm just looking at each one in a vacuum.

-

@PotatoEngineer said in 401(k) Plans No Longer Make Much Sense for Savers:

I guess I'm not quite following you when you talk about changing from post-tax to pre-tax and vice versa; I'm just looking at each one in a vacuum.

To make it simple: let's pretend I have a $19,500 annual budget for retirement savings. (AKA the annual 401(k) maximum.) I need to figure out what will work out better for me: paying tax on that amount now, or paying tax on it after retirement.

If I pay tax now, it's all going to be at that highest bracket. My average tax paid is irrelevant.

-

@Unperverted-Vixen said in 401(k) Plans No Longer Make Much Sense for Savers:

@PotatoEngineer said in 401(k) Plans No Longer Make Much Sense for Savers:

I guess I'm not quite following you when you talk about changing from post-tax to pre-tax and vice versa; I'm just looking at each one in a vacuum.

To make it simple: let's pretend I have a $19,500 annual budget for retirement savings. (AKA the annual 401(k) maximum.) I need to figure out what will work out better for me: paying tax on that amount now, or paying tax on it after retirement.

If I pay tax now, it's all going to be at that highest bracket. My average tax paid is irrelevant.

But what if you spent that money on a coke bender instead?

My point is that you don't get to pick "which bracket" post-tax money comes out of. All post-tax money is in a single pool, taxed at the average rate. Otherwise, I could just decide that it comes out of the first bracket, is taxed at 0%, and come up with a completely different decision.

Only pre-tax stuff goes into the highest bracket, because doing pre-tax spending will decrease your adjusted gross income, which always affects the money in the highest bracket; all post-tax activities have exactly zero effect on your adjusted gross income. It doesn't matter whether you spend that post-tax money on hookers, a Roth IRA, renovating, or just throw it off a cliff.

-

@Gąska said in 401(k) Plans No Longer Make Much Sense for Savers:

@apapadimoulis said in 401(k) Plans No Longer Make Much Sense for Savers:

so really your only "safe" bet is gold boolean

Isn't it already illegal to own gold in US?

"Not legal tender" doesn't mean "illegal."

-

@error said in 401(k) Plans No Longer Make Much Sense for Savers:

This thread is a roller coaster for my self-esteem about my salary.