Housing Bubbles? Is this a housing bubble?

-

@dkf said in Housing Bubbles? Is this a housing bubble?:

If you've got the income to pay down the principal rapidly, you won't have much of a problem with negative equity. But that's very much not everyone.

Again, see the example I gave of paying down the principal rapidly with $20/month. That very much is everyone; if you can legitimately qualify for a loan in the first place, you can do what my family did. I may be an affluent, successful software developer today, but as a kid I grew up in poverty. We did it anyway because we didn't want to stay in poverty.

-

@Mason_Wheeler said in Housing Bubbles? Is this a housing bubble?:

@dkf said in Housing Bubbles? Is this a housing bubble?:

If you've got the income to pay down the principal rapidly, you won't have much of a problem with negative equity. But that's very much not everyone.

Again, see the example I gave of paying down the principal rapidly with $20/month. That very much is everyone; if you can legitimately qualify for a loan in the first place, you can do what my family did. I may be an affluent, successful software developer today, but as a kid I grew up in poverty. We did it anyway because we didn't want to stay in poverty.

Yes, this sort of thing can shorten your payoff time. But you've displayed your usual reality deficit here. I've been paying $100 - $150 per month extra for a while (varies due to fluctuations in escrow) and there's nothing really dramatic about that.

-

Mods, the Garage is leaking again...

Mods, the Garage is leaking again...

-

@Mason_Wheeler sorry, I'll move those and only make fun of your financial and mathematical and organizational fantasies here.

-

@boomzilla The math of it is actually pretty cool. It goes like this:

- At the start of the mortgage, you're going nowhere very very slowly. Almost all of your standard payment is going to interest and very little is left over to actually pay down the loan.

- Therefore, if you add even a very little to your initial payments, you burn through a lot of starting time equivalent very quickly. (After 1 year of this strategy, we were 4 years into our payment schedule!)

- This speed-burndown doesn't last forever; once you get a few years into the payment schedule, you start to get diminishing returns because the interest/principal ratio of each payment decreases.

- But now you're putting a significant part of each regular payment onto the principal. This is also known as building equity.

The real cause of ending up "underwater" is that there's a big "shield" of interest-heavy payments right at the start of the mortgage schedule that prevents people from building any significant amount of equity for several years. If you can break that shield quickly and reach a point where a significant amount of your payment is going to principal, it ceases to be a problem. My point is that that is surprisingly easy to do even if you're not rich.

-

@Mason_Wheeler said in Housing Bubbles? Is this a housing bubble?:

The real cause of ending up "underwater" is that there's a big "shield" of interest-heavy payments right at the start of the mortgage schedule that prevents people from building any significant amount of equity for several years. If you can break that shield quickly and reach a point where a significant amount of your payment is going to principal, it ceases to be a problem. My point is that that is surprisingly easy to do even if you're not rich.

I agree with what you're saying generally, just that you're decades out of date on the amounts we're talking about here.

-

@boomzilla I agree that the math would be a bit different with post-2008 interest rates, but given how we're rapidly getting back to what they were in the 90s (when the house-buying in question happened) I don't think it's particularly out of date anymore.

-

@Mason_Wheeler I don’t know about the US but in the UK at least, people tend to have mortgages as a bigger percentage of their income than they did back in the 90s. So while the interest rate might be comparable, the relative pain isn’t.

-

@Mason_Wheeler said in Housing Bubbles? Is this a housing bubble?:

If you've "only" been in the house for 10 years, it should already be mostly or fully paid off.

I bought in 1996. I reached the 1/2 point in my loan in 2016. (and paid it off in 2019) I started making lots of extra payments probably around 2010.

-

@topspin said in Housing Bubbles? Is this a housing bubble?:

anything with sub

linearexponential growth is a "decrease" (if I read that correctly, we're talking about a declining percent increase here)

(if I read that correctly, we're talking about a declining percent increase here)You must be new to economics.

-

@dkf said in Housing Bubbles? Is this a housing bubble?:

prices can stay down for a long time

As they say, the market can remain rational for longer than you can stay solvent

-

@ixvedeusi said in Housing Bubbles? Is this a housing bubble?:

@topspin said in Housing Bubbles? Is this a housing bubble?:

anything with sub

linearexponential growth is a "decrease" (if I read that correctly, we're talking about a declining percent increase here)Dang it, even worse!

-

@Mason_Wheeler said in Housing Bubbles? Is this a housing bubble?:

My point is that that is surprisingly easy to do even if you're not rich.

It depends on what the loan-to-value ratio is, and what the interest rate is. The smaller the loan relative to the value, the less there is a problem because it's always possible for things to be refinanced or sold and everything wound up cleanly. But that isn't always the case. People still need to live somewhere even when it is expensive to acquire property, and the financial system accommodates this when it must. When house prices are rising, especially if they are rising faster than interest rates, it's extremely easy to do; the risk is relatively low. But if the rate of rise is lower, the risk goes up (compensated by requiring a higher downpayment — the key safety buffer in the scheme — though that significantly reduces the level of business conducted so isn't especially popular with large lenders).

It's when prices actually fall — when the market is deflationary — that things get messy. People aren't incentivized at all to enter the market (why buy this month when you can just sit tight and get more for your money) so it's harder to sell. If your money is already in property, you'll be keen to sell and get that cash somewhere else that will turn a profit. And if you're a lender, you'll see more and more of your loans under water, where you can't get all your money back even if you foreclose; the size of deposit you're going to require to ensure that won't happen is going to make people very not keen to do business with you. Overall, you get a cascading market collapse (because the impact from the people at the edge of profitability spills over to more sensible folks).

The greatest risks of this happening are in the parts of the world where prices were rising fastest. They were also the places that supported the riskiest lending when prices were going up and up and up. Market volatility is not a good sign, especially in real estate.

-

@dkf said in Housing Bubbles? Is this a housing bubble?:

The greatest risks of this happening are in the parts of the world where prices were rising fastest.

The colloquial term for this is "the bigger they are, the harder they fall." The somewhat more formal version I've heard is "when an asset bubble pops, prices go back to where they were when the bubble began, or a bit lower." And knowing that rule helps you guard against the problem you mentioned above?

People aren't incentivized at all to enter the market (why buy this month when you can just sit tight and get more for your money) so it's harder to sell.

I've got a known target: prices aren't likely to fall much below 2012 levels. So that's where I'd look to buy.

-

@Mason_Wheeler said in Housing Bubbles? Is this a housing bubble?:

I've got a known target: prices aren't likely to fall much below 2012 levels. So that's where I'd look to buy.

What people actually do, provided they're not needing to purchase immediately, is wait until a bit after prices start rising again. A simple strategy based on only gross reading of pricing signals and mostly fairly effective when prices aren't bouncing up and down. The more volatile things seem, the longer buyers wait.

If you're able to just stay put and handle the loan to the point where you own outright, negative equity is a complete non-factor, or at least only a theoretical problem (and might be covered by suitable life insurance).

-

@Mason_Wheeler said in Housing Bubbles? Is this a housing bubble?:

Again, see the example I gave of paying down the principal rapidly with $20/month.

$20/month, so $240/year, or $7200 over 30 years... How exactly does that allow to pay up even a puny $100k loan faster by a significant margin? How does the math work out here?

-

According to this page

$20 extra on 30-year $100k loan at APR 3-9% accelerates repayment by 2-3 years.

I'm starting to think the additional payments movement is a conspiracy by the financial elite to trick common people into voluntarily transfering even more of their wealth to the wealthy.

-

@Gustav said in Housing Bubbles? Is this a housing bubble?:

According to this page

$20 extra on 30-year $100k loan at APR 3-9% accelerates repayment by 2-3 years.

I'm starting to think the additional payments movement is a conspiracy by the financial elite to trick common people into voluntarily transfering even more of their wealth to the wealthy.

I've always heard "early repayment" being more like making an extra payment each month if you pay 2x/month (or an extra half-monthly payment). That is, paying 50% extra. Now that, I can believe will reduce your time to pay off. It's basically taking out a 30 year note for something you could pay in 15 but paying it like it was a 15 year note (the interest rates are different, which makes up the difference, mostly), which isn't a bad idea. Which gives you some cushion to drop back if there's unexpected expenses without actually being late on any payments.

But it's a far cry from $20/month extra.

-

@Benjamin-Hall there are different ways of extra payment. You can simply upcharge the loan account, which is what you talk about - extra money that just sits there and does nothing. For people who don't have an impulsive buying problem, this is a straight downgrade from keeping the money in your regular bank account. Another way is extra capital payment. Essentially you bump up the capital part of capital+interest that make up your monthly payment. And the lower the capital, the lower the interest. The earlier you pay, the less you have to pay overall. Whether it makes sense depends on how your interest rate compares to inflation, or if you're feeling adventurous, inflation + ROI after you put that money elsewhere. And because the money immediately goes into capital, it gives zero protection against future missed payments.

-

@Gustav that latter was what I was talking about. Making extra payments against principal, in excess of the regular so you can cut down on total interest payed. The first is, as you say, kinda bad. But the reason to take an officially 30 year loan and pay extra payments instead of a 15 year loan is that the minimum payment (regular amortization) is lower so if you hit a rough patch you can drop the extra payments and still be in good standing on the loan's normal terms.

-

@Benjamin-Hall ah, gotcha. That makes sense.

-

@Arantor said in Housing Bubbles? Is this a housing bubble?:

@Mason_Wheeler I don’t know about the US but in the UK at least, people tend to have mortgages as a bigger percentage of their income than they did back in the 90s. So while the interest rate might be comparable, the relative pain isn’t.

In a mature market, house prices are a function of interest rates and local income. That is, once prices have settled, the most expensive houses in any given area will cost exactly as much as the people there can afford to pay, interest included. And the rest of them will have a price relative to that.

Housing taking a bigger percentage of income just means food and clothing expenditures have been smaller than they were in the 90s.Now that food, clothing and heating expenses are up, housing will come down. People will default on mortgages that they can't afford to pay, and this may cause some banks to fold.

-

@Benjamin-Hall said in Housing Bubbles? Is this a housing bubble?:

@Gustav that latter was what I was talking about. Making extra payments against principal, in excess of the regular so you can cut down on total interest payed. The first is, as you say, kinda bad. But the reason to take an officially 30 year loan and pay extra payments instead of a 15 year loan is that the minimum payment (regular amortization) is lower so if you hit a rough patch you can drop the extra payments and still be in good standing on the loan's normal terms.

Yup. The only drawback is that the interest is lower on a 15-year loan than on a 30-year loan. But having that extra cushion is pretty nice.

(The bonkers part is that 20, 25, and 30 year loans all have roughly the same interest rate, with teeny-tiny improvements in 20 and 25, and then there's a bigger drop in interest at 15 years (.25%-.5% lately).)

-

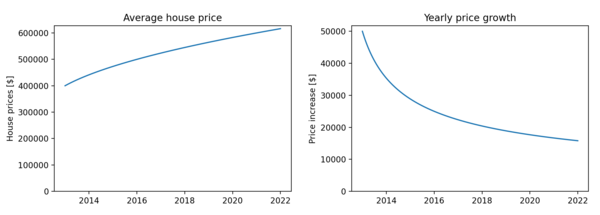

@topspin said in Housing Bubbles? Is this a housing bubble?:

@boomzilla said in Housing Bubbles? Is this a housing bubble?:

Home prices are falling at a record pace

Despite the nationwide trend of falling home pricesPrices are still up for the year, but the percentage keeps dropping each month. The S&P CoreLogic Case-Shiller Index, which tracks national home prices, reported annual gains at 13% in August, marking a decline from 15.6%

S&P also reported that the 10-City Composite annual increase fell from 14.9% in July to 12.1% in August, while the 20-City Composite annual increase fell from 16.0% to 13.1%. The largest declines in housing prices came from San Francisco, Seattle, and San Diego.So which is it? A "declining increase" is not a decrease. The prices are still rising.

According to them, anything with sublinear growth is a "decrease". Here's a quick mock-up of what they call declining prices:

Everybody know the way to make real money these days is trading in derivatives

-

@PotatoEngineer said in Housing Bubbles? Is this a housing bubble?:

and then there's a bigger drop in interest at 15 years (.25%-.5% lately).)

That's about as much as the normal week-to-week market fluctuations. It adds up to about 3-6k of 30-year interest per 100k of capital. Totally not worth it.

-

@Gustav said in Housing Bubbles? Is this a housing bubble?:

@PotatoEngineer said in Housing Bubbles? Is this a housing bubble?:

and then there's a bigger drop in interest at 15 years (.25%-.5% lately).)

That's about as much as the normal week-to-week market fluctuations. It adds up to about 3-6k of 30-year interest per 100k of capital. Totally not worth it.

Depends. My last refi was to a 15y. I had about 20 or 25 years left on the previous 30. My monthly payment actually dropped slightly.

-

@dcon said in Housing Bubbles? Is this a housing bubble?:

@Gustav said in Housing Bubbles? Is this a housing bubble?:

That's about as much as the normal week-to-week market fluctuations. It adds up to about 3-6k of 30-year interest per 100k of capital. Totally not worth it.

Depends. My last refi was to a 15y. I had about 20 or 25 years left on the previous 30. My monthly payment actually dropped slightly.

That's comparing it to the rate on your former 30 year mortgage, not what the rate on a new 30 year mortgage would be.

-

@Mason_Wheeler said in Housing Bubbles? Is this a housing bubble?:

- insanely long-term mortgages

Hmmm.. for my residences, I have used 15 year mortgages, paid them in full early also.... Now for investment properties it is all about timing the gains, so different equations...

-

The view to die for is about 35seconds in

-

-

@GOG said in Housing Bubbles? Is this a housing bubble?:

@loopback0 said in Housing Bubbles? Is this a housing bubble?:

view to die for

So you're saying you have grave problems with that joke?

-

@loopback0 You're basically volunteering to always be the host for Halloween parties.

-

@dkf He wouldn't be caught dead using it.

-

@cvi The neighbours seem pretty chill, though.

-

@GOG a congenial location for certain experiments, necessary to the advancement of the species but abhorrent to the common, indeed.

-

A saudi-arabian prince became broke, and now his home in London is for sales. Expected price somewhere around 250 million quids.

Article in the FAZ in German (perhaps someone finds an english article,

):

):

In London steht das Luxusanwesen „The Holme“ zum Verkauf

In London steht das Luxusanwesen „The Holme“ zum Verkauf

Das teuerste Anwesen Londons steht zum Verkauf. Der Eigentümer, ein saudischer Prinz, ist insolvent. Der Fall wirft ein Schlaglicht auf einen Häusermarkt, auf dem die Stadtbewohner keine Rolle mehr spielen.

-

https://archive.ph/kHvqx UK’s most expensive house: London mansion on sale for £250m

UK’s most expensive house: London mansion on sale for £250m

A Saudi prince has put a London mansion on the market for £250 million in what would be the most expensive property sale ever in Britain.The Holme, built in 181

-

-

Here's a factor I hadn't previously considered:

Winning college football teams drive up rents

This is pretty funny. From DNYUZ: How College Football Is Clobbering Housing Markets Across the Country December 18, 2023 Rashe Malcolm loves her son Wayne and his girlfriend, but she’d also love it if they could move out of the three-bedroom home in Athens, Ga., that she shares with the couple,...

Around the United States, in small cities reliant on college sports to keep their economies humming, short-term rentals are destabilizing housing markets, fueled by wealthy fans and investors who transform single-family homes into de facto hotels for a few weeks out of the year, and often leave them sitting empty the rest of the time.

-

Home Prices Hit a High in 2023. Limited Supply Continues to Fuel Gains.

Home Prices Hit a High in 2023. Limited Supply Continues to Fuel Gains.

Prices gained 6.1% in December from a year ago, Case Shiller says..

-

Check out this Studio flat for rent on Rightmove

Studio flat for rent in New Street, Dudley, DY1 for £725 pcm. Marketed by Taylors Estate Agents, Brierley Hill

The building's a former police station. The holding cell is left in this studio flat as a feature.

Key features

LARGE STUDIO WITH FEATURE HOLDING CELL

-

@loopback0 said in Housing Bubbles? Is this a housing bubble?:

Studio flat for rent in New Street, Dudley, DY1 for £725 pcm. Marketed by Taylors Estate Agents, Brierley Hill

The building's a former police station. The holding cell is left in this studio flat as a feature.

Key features

LARGE STUDIO WITH FEATURE HOLDING CELL

The lifestyle thread is

-

@loopback0 said in Housing Bubbles? Is this a housing bubble?:

Studio flat for rent in New Street, Dudley, DY1 for £725 pcm. Marketed by Taylors Estate Agents, Brierley Hill

The building's a former police station. The holding cell is left in this studio flat as a feature.

Key features

LARGE STUDIO WITH FEATURE HOLDING CELL

Perfect for teenage daughters!